Anatomy of a (fake) Market

Most $CEL trading volume on Uniswap is wash trading. And we can prove it!

Over the last few months, Dirty Bubble Media has documented the various questionable and potentially fraudulent aspects of the crypto lending firm Celsius Network. We’ve previously shown that their CEO has a tenuous relationship with the truth, that their business model is (at best) a hyper-risky Rube Goldberg debt machine, and that their proprietary token $CEL shows many hallmarks of market manipulation.

Recently, we decided to perform a detailed analysis of $CEL trading on a decentralized exchange (DEX), Uniswap. The $CEL/$WETH spot market on Uniswap is the 5th-largest market for $CEL, comprising ~12% of total trading volume:

While Uniswap is far from the largest market for $CEL, its decentralized structure allows us to examine every transaction that occurs via the contract. While we have demonstrated likely manipulation on centralized exchanges like FTX in the past, these analyses fell short of a “smoking gun” that conclusively proved manipulation was occurring.

Here, we demonstrate that at least 59% of $CEL token volume on this exchange is wash trading, which is a type of market manipulation aimed at creating the illusion of organic demand. Wash trading is an illegal form of market manipulation per the Commodities Exchange Act.

For this analysis, we examined all $CEL/$WETH swaps on Uniswap V3 over the period of 3/21/22 to 3/26/22. We restricted it to this period for ease of analysis, as longer periods would have thousands of transactions. However, this smaller dataset is sufficiently representative to draw robust conclusions (1).

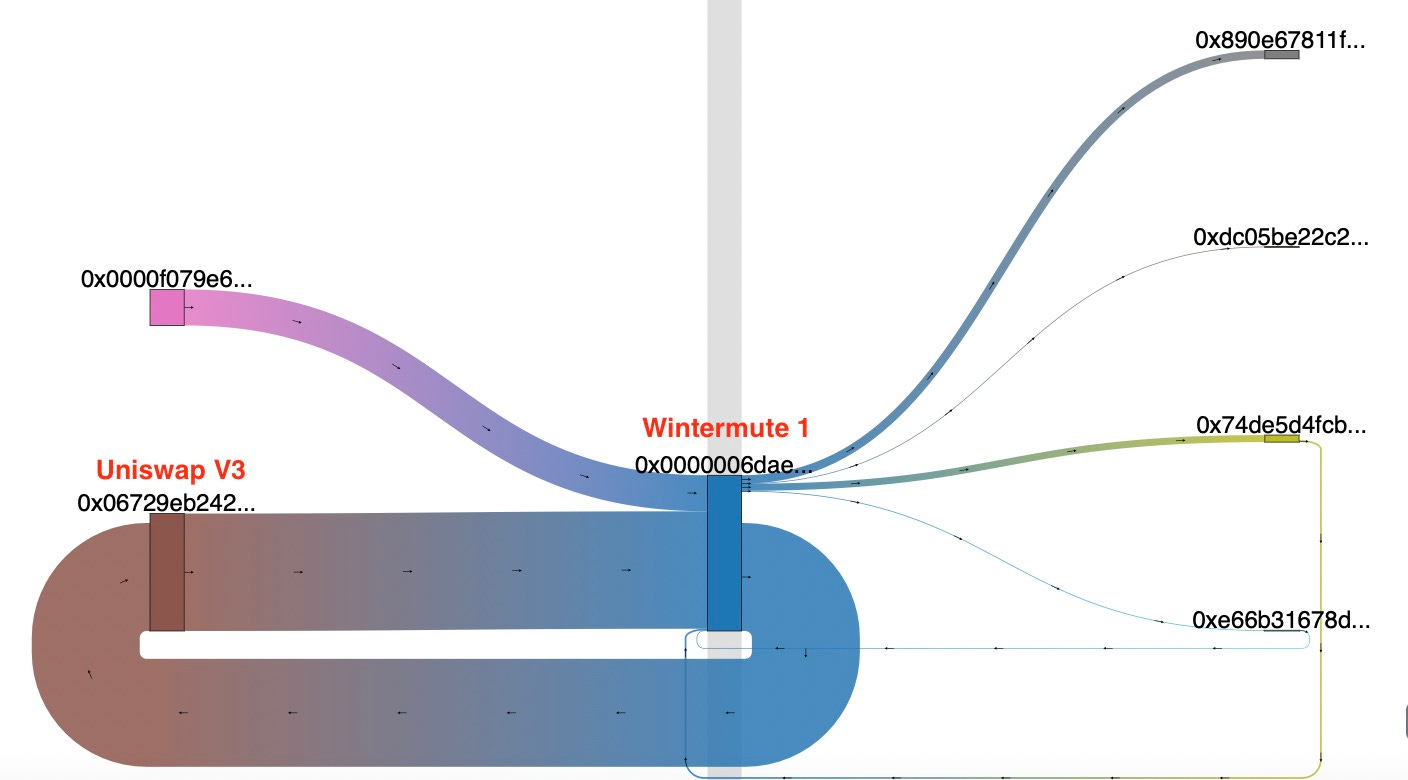

Wintermute: Based on these data, 47% of $CEL swaps (WETH for CEL) are performed by Wintermute, a “leading global algorithmic market maker in digital assets.” In traditional markets, a market maker facilitates the purchase and sale of assets, acting as a middle-man between third parties. However, in crypto-land, market maker has a different meaning; quite literally, “making” the market. Wintermute regularly swaps $CEL, and its other clients’ tokens, in and out of DEXs to create the appearance of demand, AKA wash trading:

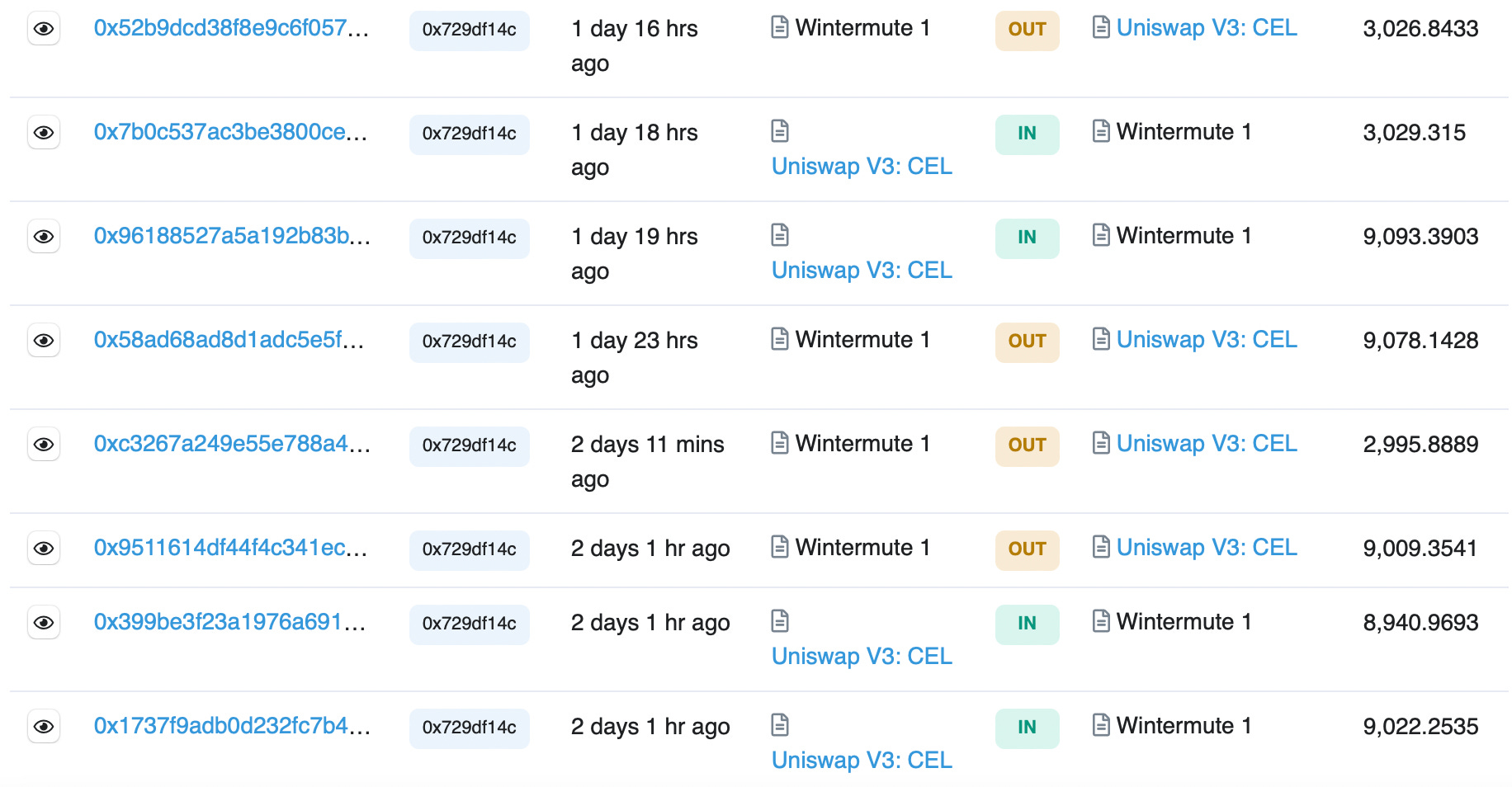

Wintermute’s $CEL trades are far larger than the average trade on the market, typically several thousand $CEL per trade. These trades are balanced over a few hours; Wintermute swaps $CEL into Uniswap, then shortly after swaps the same amount back out:

To reiterate: This is NOT simply “providing liquidity,” as the size of these trades is far above the average trade executed by the wallets we believe to be legitimate. When providing liquidity is nearly half of an entire market… it’s wash trading.

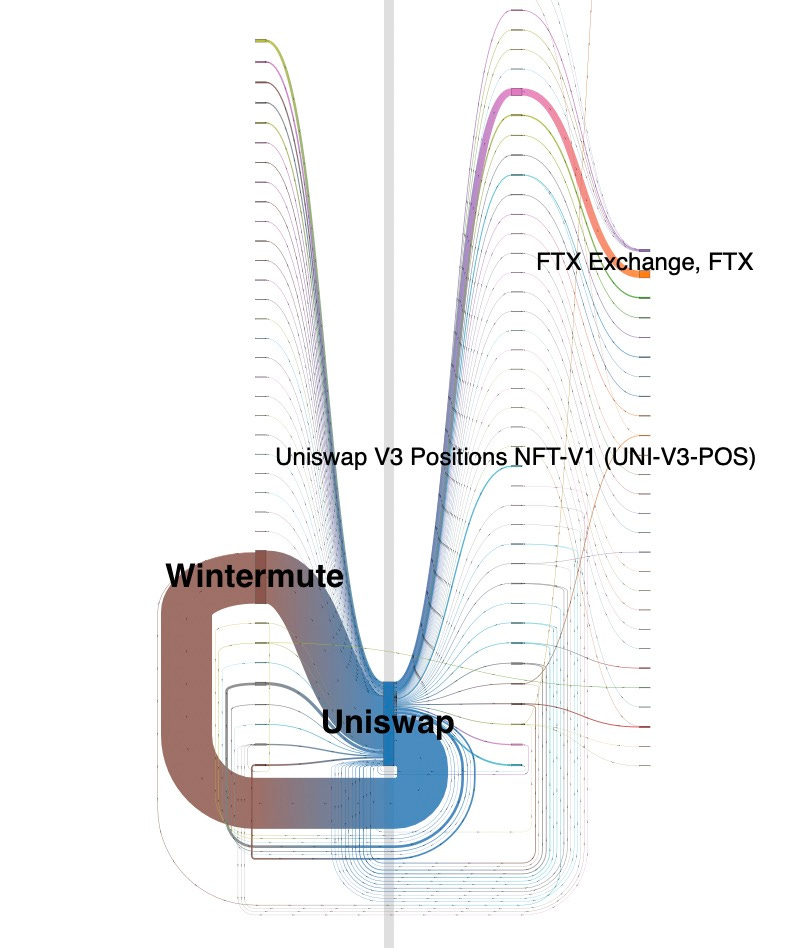

FTX: After Wintermute, the next-largest fraction of $CEL token travels directly from Uniswap to the FTX exchange, host of the largest spot market for CEL ($CEL/$USD). This wallet executes large swaps for thousands of CEL, then immediately transfers the tokens to FTX:

We have previously documented the relationship between FTX and Celsius, as well as the features of the CEL/USD market that suggest most of the CEL trading volume on FTX is on Celsius’ behalf. We strongly suspect that these transactions also represent a type of wash trading, where $CEL token is shifted between different exchanges to create the illusion of demand.

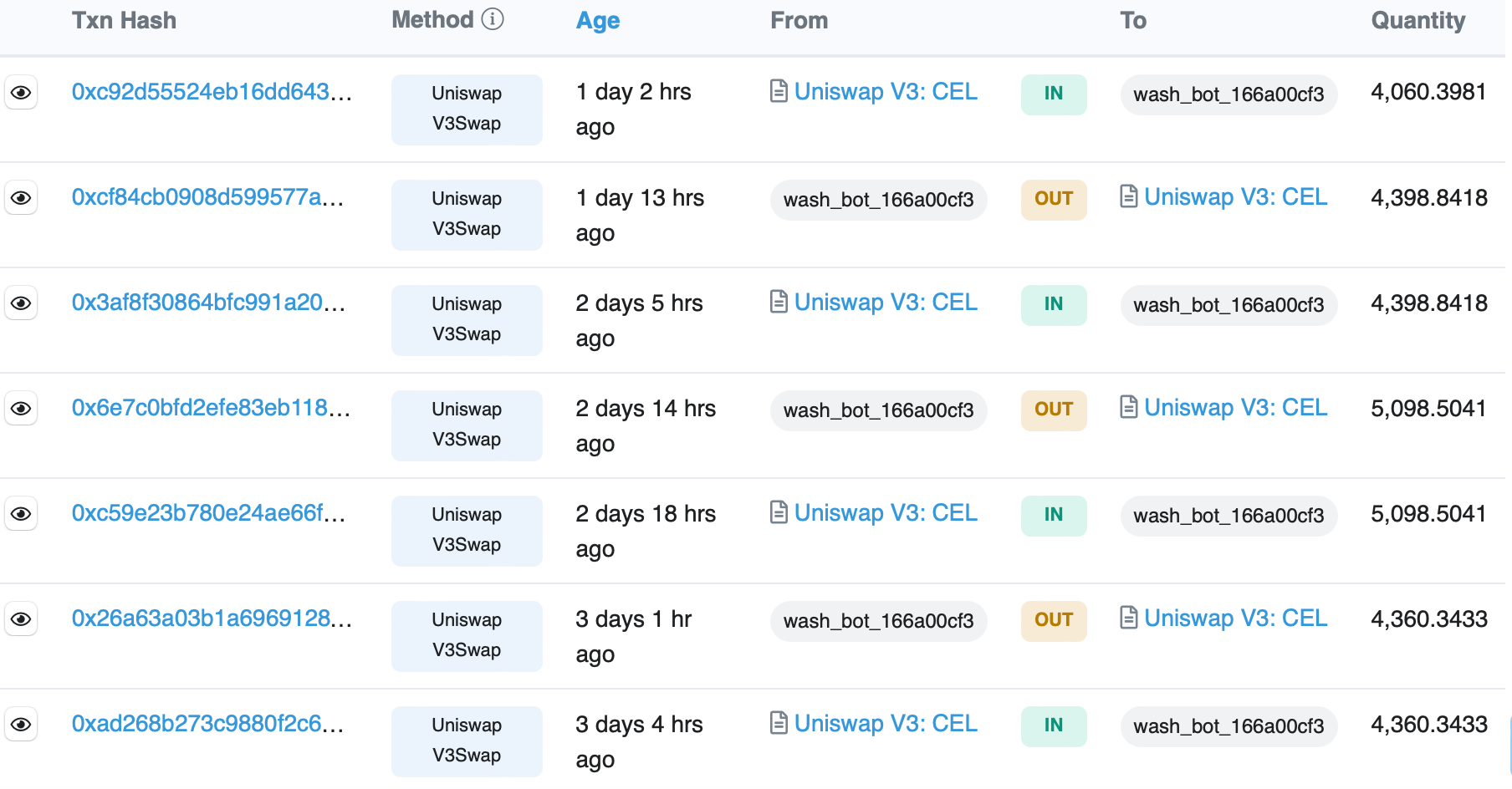

Wash Trading Bots: An additional 12% of the CEL/WETH volume on Uniswap is attributed to several wallets that engage in obvious wash trading. These wallets buy and sell balanced amounts of CEL over periods of several hours in a pattern that is similar to the one demonstrated (on a larger scale) by Wintermute. Some of them transfer CEL between different DEXs, while others transact only on Uniswap.

Other volume: While there is obviously a significant amount of fake trading going on, there appears to be some real activity occurring. 9% of CEL swap purchases were by wallets that are likely controlled by individuals (or, at least, we could not show otherwise). These wallets then transferred their CEL to Celsius Network Wallet 5. Another 9% of volume was attributed to other unidentified wallets with no clear relationship to Celsius. 6% of volume were apparently transfers of CEL to the 1inch DEX, and 5% (a large, single trade) was executed by the “0x Exchange Proxy Flash Wallet.”

Conclusion: Based on these data, we conclude that at least 59% of CEL/WETH volume on Uniswap from 3/21-3/26/22 was wash trading. Nearly half of the total volume came from a single “market maker,” with an additional 12% generated by other obvious wash-trading wallets.

Based on our previous observations of CEL trading on FTX, it would be reasonable to include these transfers under the category of wash trades. Further, the trades between Uniswap and the 1inch DEX exchange may also represent “market faking” activity. In total, this means that conservatively 75% or more of the CEL/WETH volume on Uniswap represents fake demand for CEL token. This would be in line with previous studies showing that ~70% of crypto trading is likely wash trading.

(1) Below is an illustration of CEL flows through Uniswap over the last month. You can observe that the majority of tokens make a round-trip through either Wintermute or several other wallets back to Uniswap, with a significant remainder heading to FTX. While the precise percentages will vary, this demonstrates the overall conclusion above- the majority of CEL trading activity goes in a circle rather than representing legitimate demand:

hi, which software do you use to create the flow charts? thx.