Celsius Liquidated User Assets to Pay DeFi and FTX Loans

As crypto flowed to FTX, over $1 Billion in USDC came back in...

There was a one-month period between Celsius Network freezing withdrawals and filing for Chapter 11 bankruptcy protection (“The Freeze”). During that period, and a little before, Celsius made net transfers of over $700 million worth of Bitcoin, Ether, MATIC, LINK, and other crypto to the FTX exchange. In addition, Celsius had previously sent $403 million of crypto to FTX as collateral for a $108 million loan. In the same period, Celsius received $1 billion in USDC from FTX and the $108 million loan from FTX was discharged.

Around the same time, $938 million worth of Celsius’ Bitcoin was liquidated by Tether to pay back an $841 million loan.

I reconcile blockchain flows to Celsius’ balance sheet, obtained from bankruptcy filings, and show striking similarities between Celsius’ crypto losses and assets transferred during this period. Together this data strongly suggests that Celsius liquidated user assets, previously used as collateral for loans from decentralized finance (DeFi) platforms, to pay off those DeFi loans.

Additionally, I show that the hole in Celsius Network’s balance sheet prior to the freeze period was primarily in the form of dollars Celsius had borrowed. This raises an interesting question: What did Celsius do with the $2.4 billion dollars in stablecoins that they borrowed from DeFi, FTX, Tether, and their customers? Why did Celsius need to liquidate user crypto to pay these debts, instead of pulling dollars back from the various investments or loans they had made?

Before the freeze, Celsius had borrowed $1.6 billion from DeFi, FTX, and Tether

Celsius was always hungry for dollars. To convert crypto they had received from customers into dollars, they “rehypothecated” these assets by borrowing stablecoins against them. These loans were overcollateralized. For example, Celsius borrowed somewhere around $1 billion from Tether in 2021. As collateral, they provided Bitcoin worth substantially more than that (at least 30% overcollateralized per comments from Alex Mashinsky). Celsius could then use the dollar equivalent stablecoins (USDT, USDC, DAI) to fund loans to institutional partners, pay operating expenses, engage in trading themselves, and who knows what else!

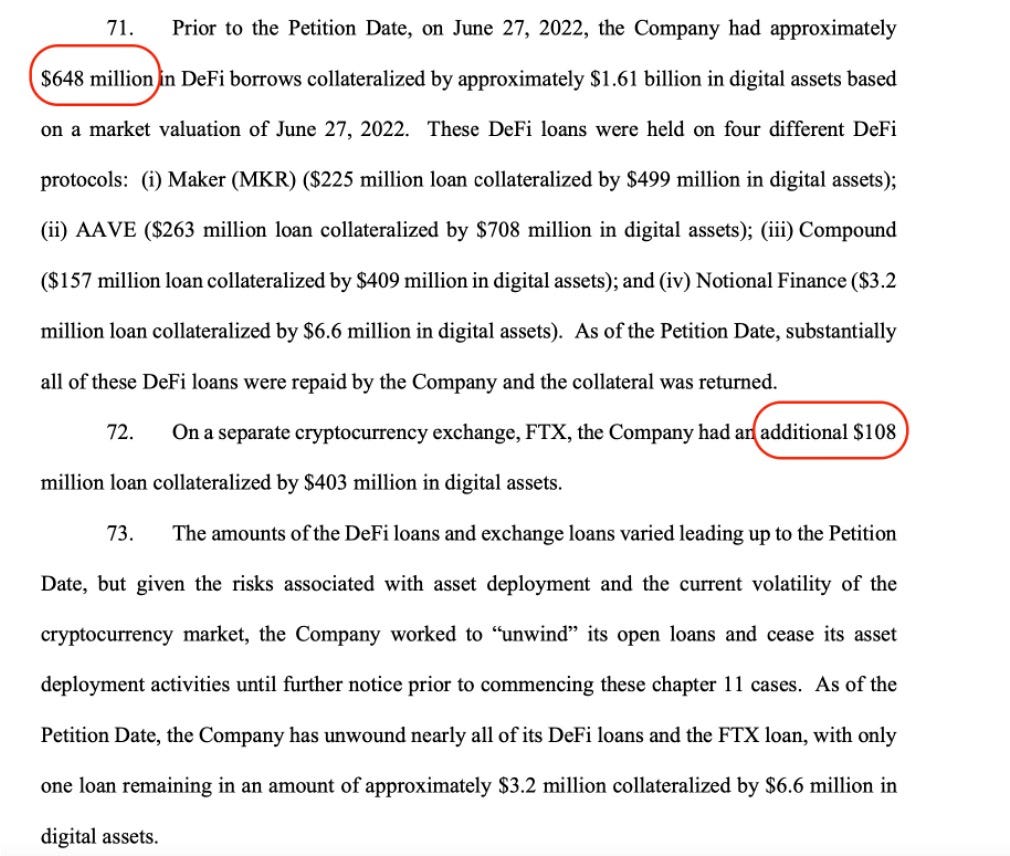

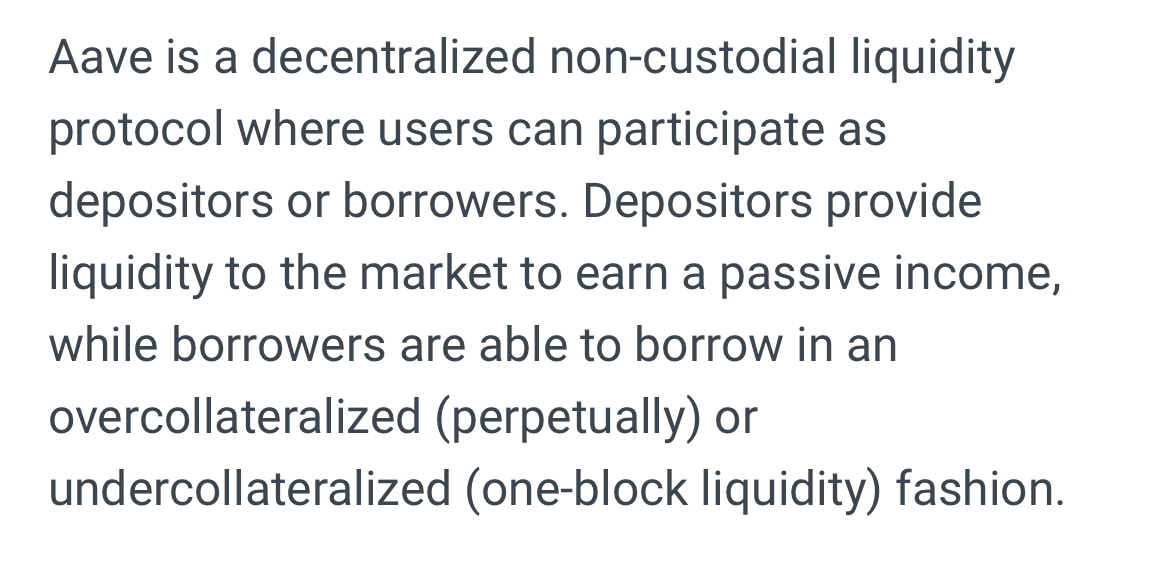

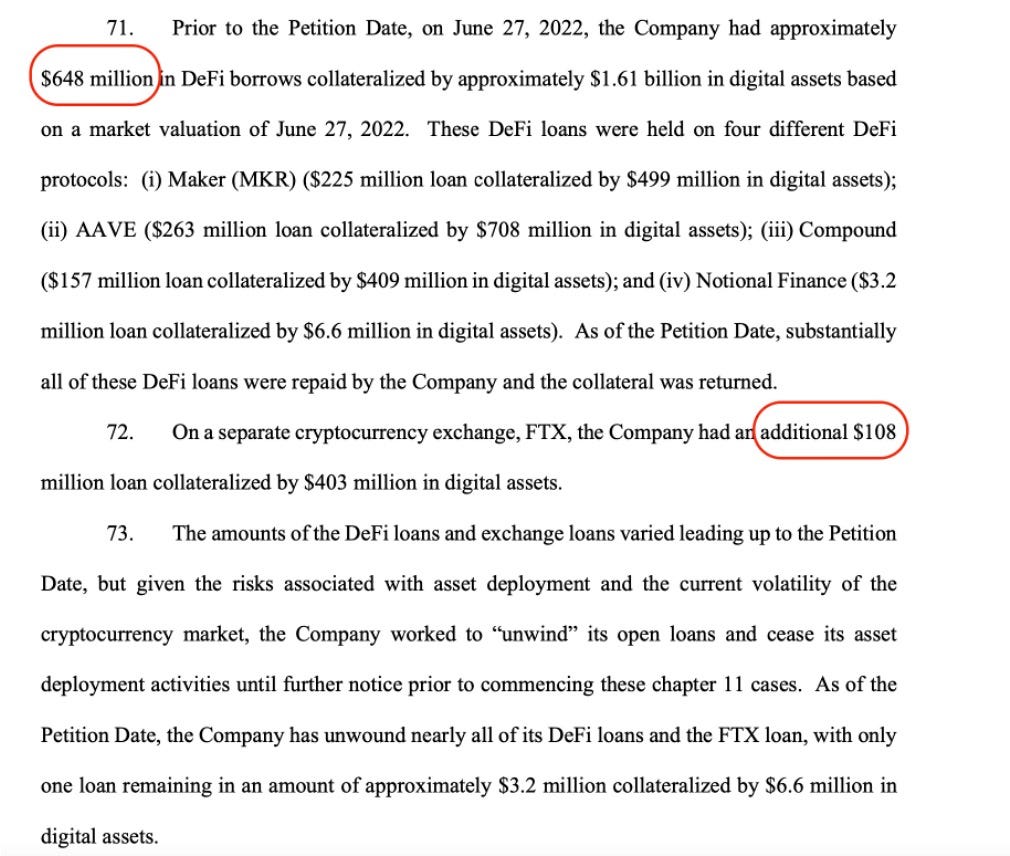

According to the Mashinsky Declaration, one of the first filings in the Celsius Chapter 11 bankruptcy, Celsius had also borrowed $648 million from decentralized finance (DeFi) protocols like Maker, Aave, and Compound. Basically, you can understand these protocols as a very simple bank. If you “stake” your asset in the pool, you can earn a return on your “deposit.” Other people pay interest to borrow those assets, but must have deposits on the platform to serve as collateral:

Celsius Network decided to begin depositing some of their user assets as collateral on these protocols, borrowing stablecoins in return. By the time of the withdrawal freeze in June, Celsius had hundreds of millions of dollars worth of debt on these platforms.

Finally, Celsius owed the FTX exchange $108 million which was collateralized with $403 million in crypto assets.

Celsius paid off at least $756 million in DeFi and FTX loans in the 45 days before Chapter 11

Celsius was in a bind. They had overcollateralized loans on these protocols, and there was some speculation that if crypto prices fell low enough their positions could face partial liquidation. (It’s worth noting that crypto prices never fell enough to make this possibility a reality, so it’s reasonable to conclude that Celsius may have panic-sold some assets to pay down these loans… regardless.)

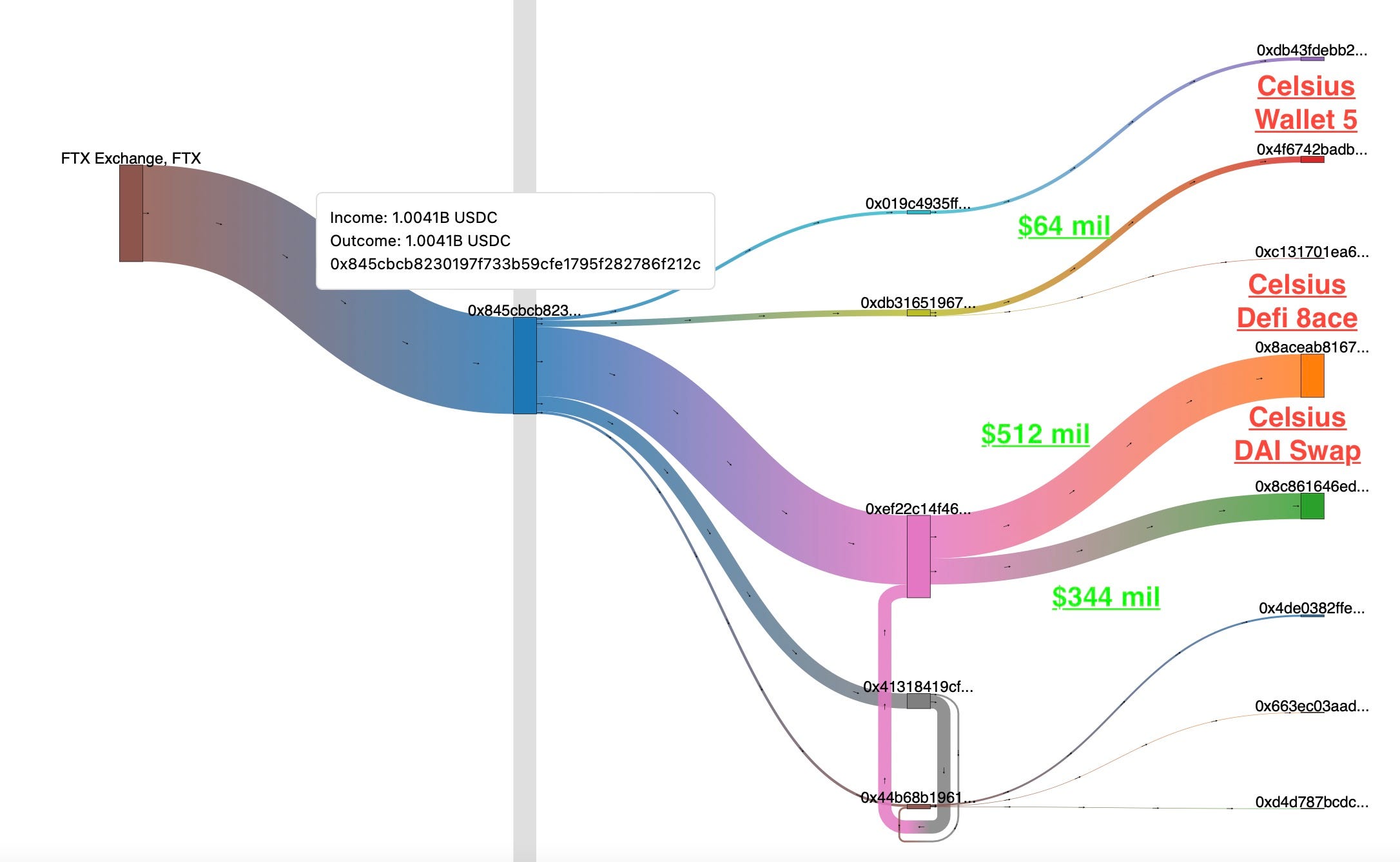

Celsius began making significant payments on these debts around June 1. Coincidentally, this is the same time FTX began sending massive amounts of USDC to Celsius Network. All told, between June 1 to July 13th, FTX sent Celsius just over $1 billion worth of USDC:

Where did the funds go?

$512 million flowed to Celsius’ DeFi wallet 0x8aceab…, now called Celsius Network Wallet 11 by Etherscan. These funds were used to pay down debt on Aave and Compound, with some sent to the DAI swap wallet

$344 million flowed to a wallet used by Celsius to swap USDC for the DAI stablecoin. This was then used to pay down DAI-denominated debt on Compound and Celsius’ Maker position

You will note that the total debt paid back on-chain is more than the Mashinsky declaration figures. This is likely due to the constantly fluctuating amount of debt Celsius held on these platforms. Celsius would regularly borrow from one DeFi protocol to pay loans on another protocol, making it difficult to determine net flows. At a minimum, we know that at least $648 million in debt was paid during this period to Maker, Aave, and Compound. Another $108 million debt to FTX was discharged.

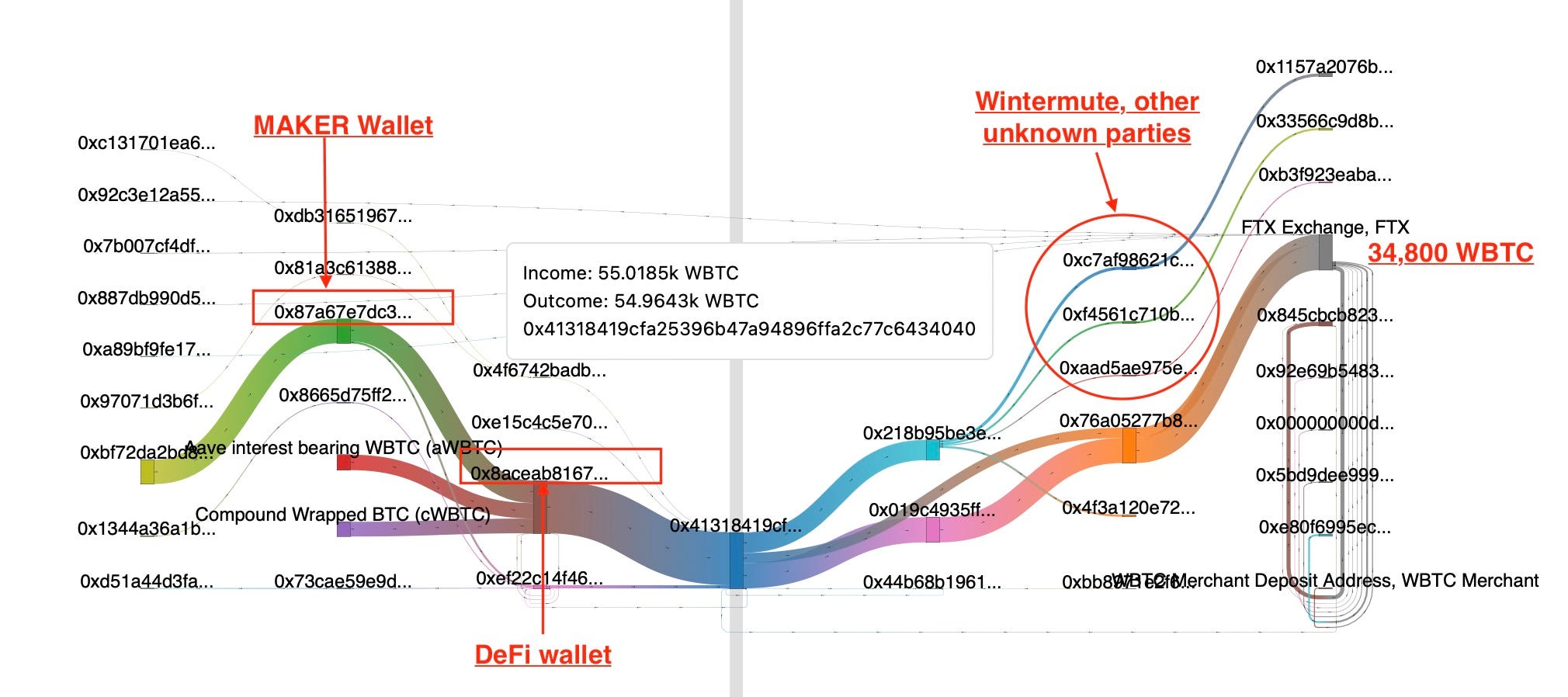

Celsius Network Transferred 55,000 WBTC during the freeze. Somewhere between 17,000 to 31,000 never came back.

Regardless of the merits or demerits of Bitcoin, everyone can agree that there isn’t much you can do with Bitcoin besides transfer it between wallets. The Ethereum blockchain allows for much more flexibility, including creating things like DeFi protocols. So how do you make your Bitcoin assets, which are on the Bitcoin blockchain, over to the Ethereum blockchain?

“Wrapping” allows users to hop assets across blockchains. For example, you can deposit Bitcoin on the Bitcoin blockchain to addresses controlled by the Wrapped Bitcoin Network. This entity then stores your Bitcoin and issues tokens on the Ethereum chain that are “backed” by Bitcoin. These “wrapped Bitcoin” are then treated as equal in value to the original Bitcoin and can be used on the Ethereum chain like any other ERC20 token. Celsius could then used these wrapped Bitcoin (WBTC) as collateral on DeFi protocols and borrow stablecoins.

During the freeze period, Celsius paid back its loans to Maker, Compound and Aave. At the same time, Celsius pulled WBTC collateral out of these protocols. A total of 55,018 WBTC were removed from Aave, Compound and Maker (total ~$1 billion):

Of these, 34,800 WBTC were sent directly to the FTX exchange. The largest single transfer was for 27,362 WBTC; this was primarily drawn from Celsius’ Maker DAO account.

During the same period, FTX transferred 18,300 WBTC back to Celsius Network. 10,600 of those WBTC are still held in a Celsius wallet; another 7,600 were sent to Celsius DeFi positions, then later withdrawn and sent back to FTX. This means that net, Celsius sent FTX ~16,500 WBTC, equivalent to roughly $325 million.

In the three days before filing for chapter 11 (7/10 - 7/13), an additional 8,000 WBTC ($160 million) were sent from Celsius to several wallets. We have identified the recipients as the Wintermute market maker (known to have been working with Celsius) and addresses linked to Alameda Research (FTX’s hedge fund) and Genesis:

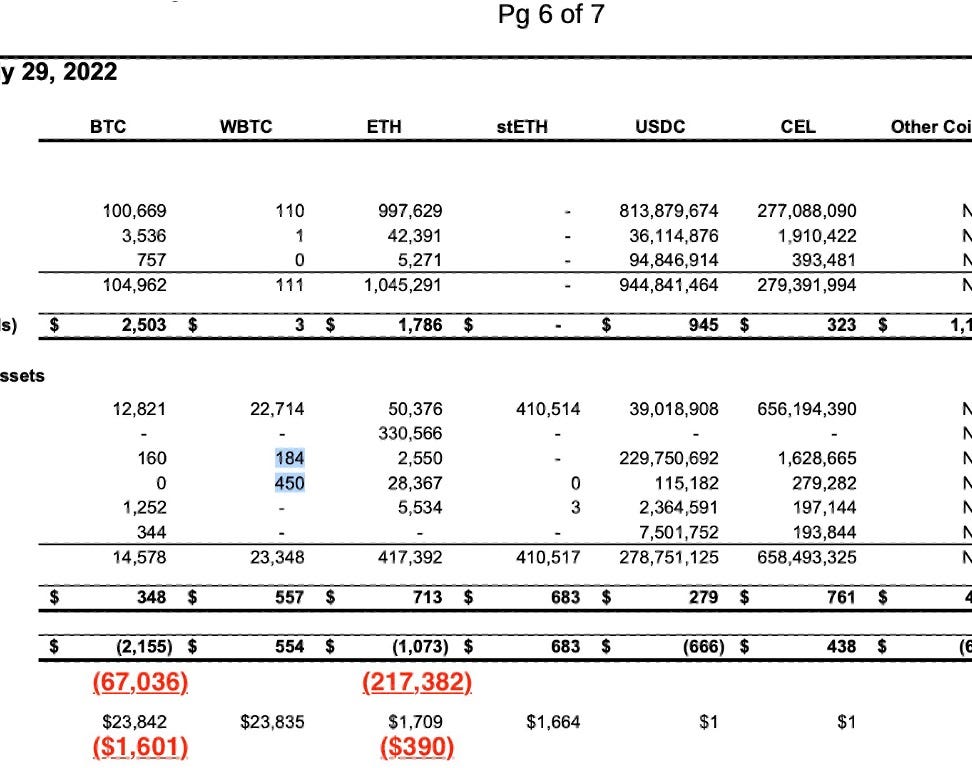

All told, somewhere around a net 50,000 WBTC were transferred from Celsius Network addresses during the freeze period. Yet, per Celsius’ own balance sheet, they currently only own a total of 37,927 Bitcoin. 23,348 are held as WBTC, with the remainder held as Bitcoin on the Bitcoin blockchain:

Now, conservatively, it is possible that all of Celsius’ Bitcoin were WBTC during the freeze and some of the WBTC transferred out of Celsius’ wallets ended up being unwrapped and sent back to Celsius regular Bitcoin wallets. This would mean that conservatively around 17,000 Bitcoin evaporate from Celsius’ wallets during the freez; it is interesting how close this number is to the net flows of 16,500 WBTC to FTX! More liberally, as much as 31,000 WBTC were lost in the freeze period.

Celsius is short approximately 67,000 Bitcoin in total. I estimate somewhere between 30,000 to 35,000 Bitcoin were lost in the Tether liquidation. It appears that Bitcoin lost during the freeze account for somewhere between half, to nearly all, of the remaining missing Bitcoin.

Celsius Had 460,000 stETH. After June 8th, they only have 410,000 stETH.

Celsius had made the controversial decision to “stake” large amounts of their customers’ Ether in the Eth2 contract. Of these staked Ether, 460,400 were staked using the Lido protocol. Lido holds the keys to the locked Ether, and then issues a “staked Ether” token that trades at an equivalent price to one Ether. Celsius was then able to simultaneously stake its Ether, then could use the stETH derivative as collateral to borrow stablecoins. Around the time of the freeze, all of Celsius’ stETH was staked on Aave as collateral.

On June 8, 2022, Celsius withdrew 50,000 stETH from Aave, and sent it on its merry way to FTX. At the time of transfer, this would have been worth roughly $90 million.

Celsius later transferred the remaining 410,000 stETH to another Celsius wallet after paying off their Aave debt. Today, per Celsius’ bankruptcy filing, they own 410,514 stETH, confirming that 50,000 stETH never came back from FTX:

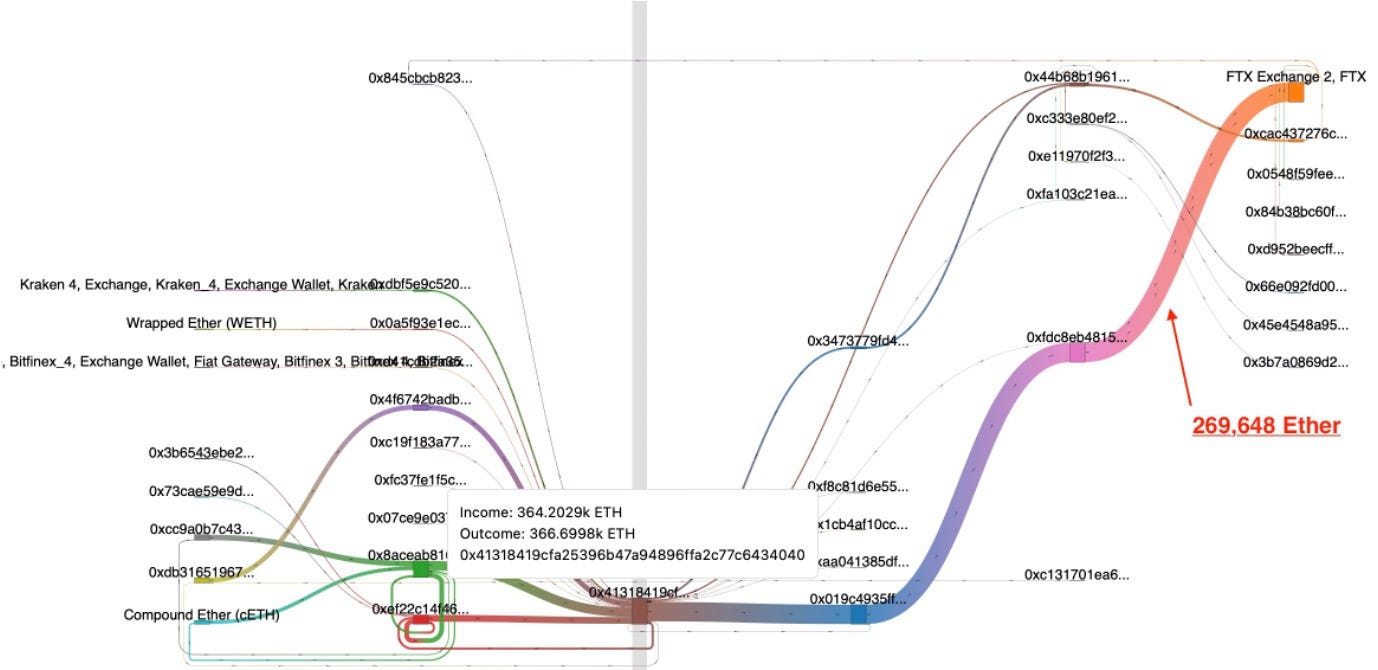

Celsius has 50,376 unstaked Ether in its wallets today. They sent 269,464 Ether to FTX during the freeze.

In addition to 460,000-odd Ether staked through the Lido service, Celsius had staked an additional 330,566 Ether directly in the Eth2 contract. Ether staked in the Eth2 contract are “locked;” you can think about it like a certificate of deposit, except it is literally impossible to withdraw before the unlocking date. This left a relatively small amount of Ether free; much of this was being used as collateral in DeFi as well.

Between June 1 and July 13, Celsius transferred 269,464 Ether to FTX:

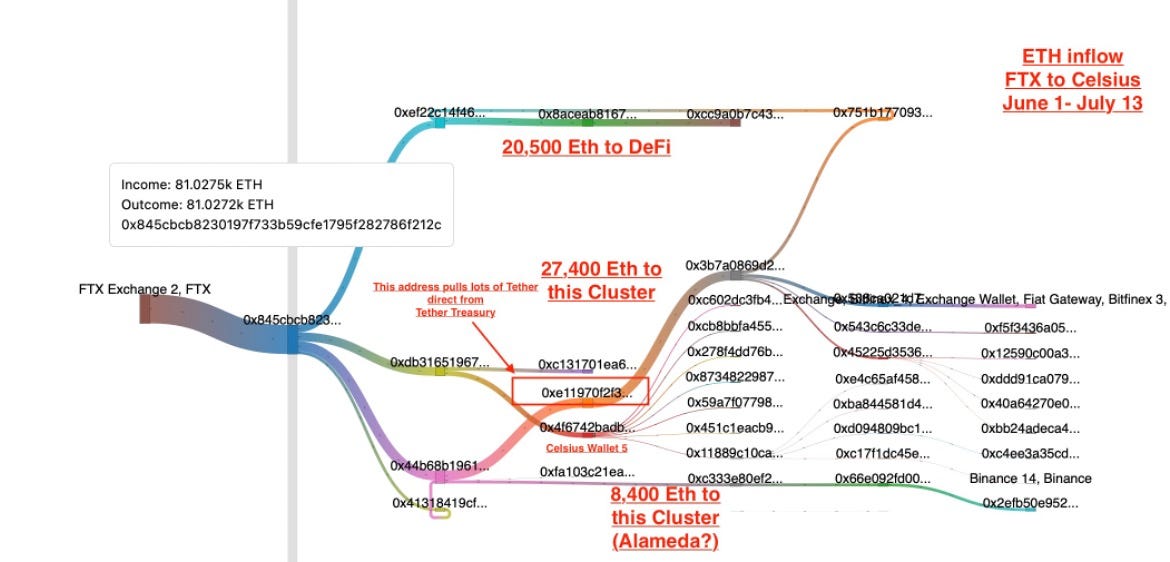

In the same period, Celsius received 81,027 Ether from FTX. 20,500 was used as DeFi collateral and transferred back to FTX later. 14,600 Ether was sent to Celsius Wallet 5 and appears to be used to fund customer withdrawals. Another 35,800 Ether ends up going to unidentified wallets. 27,400 goes to an unknown address that has directly minted Tether from the Tether Treasury (this is relatively rare). 8,400 goes to another cluster with addresses I have identified as likely belonging to Alameda Research:

Today, Celsius only holds 50,376 unstaked Ether in its wallets. It apparently held well over 260,000 Ether prior to the freeze. By their balance sheet, Celsius Network is short 217,862 Ether. Celsius sent at least 249,000 Ether to FTX during the freeze period. This suggests that most of the deficit in Ether was the consequence of liquidating assets during the freeze.

Somewhere around $250 million Ether appears to have been liquidated via FTX during the freeze period (today $350 million).

Celsius liquidated over $85 million worth of $MATIC and $LINK during the freeze

In addition to their major holdings of Bitcoin and Ether, Celsius Network accepted many other types of crypto collateral. Two of the largest types, by total AUM, were MATIC (Polygon) and LINK (Chainlink).

MATIC acts as the Ethereum token for the Polygon Network. You can stake MATIC in the Polygon contract and get paid returns on those staked assets. Celsius had done exactly this with their customers’ deposits, staking nearly all of their MATIC AUM. This meant that, unlike most of their other assets, Celsius’ MATIC was unencumbered by any debts.

Celsius withdrew 158 million MATIC from their wallets during the freeze period. 131 million were sent to FTX (worth somewhere around $65 million during the freeze). Matic was worth around $0.50 during this period; today worth closer to $0.80.

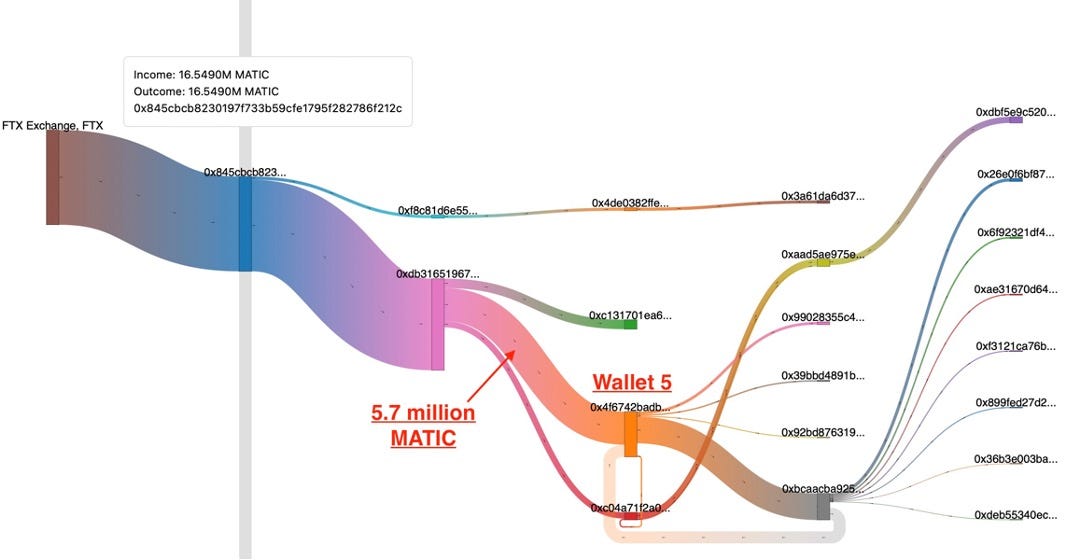

In the same period, Celsius received 16.8 million MATIC from FTX ($8.5 million). Most of these funds were sent to Celsius Wallet 5, and appear to have been used to fund withdrawals:

So net, Celsius sent at least 115 million MATIC ($65-70 million) to FTX. Per Celsius’ balance sheet, they own $74.3 million MATIC (roughly 92 mil MATIC by today’s value) and owe $204 million (roughly 255 million MATIC). This is a deficit of approximately 160 million tokens. Again, it appears a large chunk of the deficit in MATIC appears during the freeze…

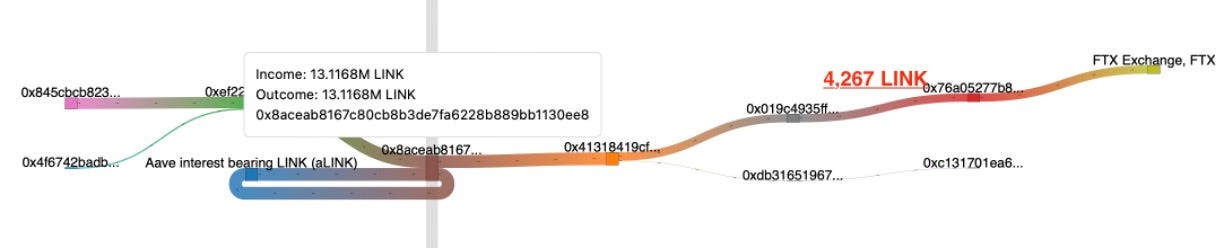

Conversely, LINK was being used as collateral for loans on Aave and Maker. Net, Celsius transferred around 4,267 LINK to FTX during the freeze period. The funds take an odd path. Celsius initially sends 6.2 million LINK to FTX on 6/18/22; then pulls those funds back to a different Celsius wallet. The LINK are transferred to their main DeFi wallet and used as collateral on Aave until 6/28, when the LINK were withdrawn again. 4.26 million are sent to FTX with the remainder staying in Celsius addresses. This would be worth around $20-25 million at the time of the freeze.

Don’t forget the other $403 million…

In addition to the over $700 million in crypto that Celsius Network sent FTX during the freeze period, Celsius had already transferred $403 million in crypto collateral to FTX as backing for a $104 million loan:

Fascinating to note how close we are getting to a balanced checkbook, here. If we add up the net funds sent to FTX, plus the collateral already held on the exchange, we get roughly $1.1 billion. Celsius received $1 billion USDC from FTX in the same period and discharged the $108 million loan. Maybe it is just a coincidence, but seems like a pretty close fit, no?

At least $360 million in crypto collateral from customers was liquidated 90 days prior to bankruptcy

Celsius’ bankruptcy filings include information about user withdrawals and loan liquidations over the 90 days prior to bankruptcy. Over the 90 days prior to bankruptcy, Celsius liquidated customer loan collateral for a total of $360 million; approximately $300 million of which was in Bitcoin or Ethereum. Another $25 million CEL, $10 million MATIC, and $3.6 million LINK was liquidated. Of this total, $254 million was liquidated during the Freeze! Celsius received another $39 million in loan repayments during the Freeze period.

Coda: Where is the $2.4 billion Celsius Network borrowed?

Between their loans from Tether, FTX, and DeFi, celsius had borrowed over $1.6 Billion. Additionally, per their balance sheet, Celsius owes customers some $780 million in USDC, USDT and Gemini USD stablecoins. This means that Celsius had borrowed around $2.4 billion in stablecoins.

However, they appear to have lost these assets along the way! They were not able to pull back the dollar equivalents to pay back their debts. Instead, Celsius had to liquidate other users crypto to pay back loans from Tether, FTX and DeFi. They still owe their own customers over $780 million in dollar equivalents.

Where did the dollars go?

Wow...FanFreakingtastic article of mapping and sleuthing! You have a special skill and a stellar way of explaining that skill. Loved it. Thank you!