Crypto Bank Whack-A-Mole

One by one, regulators are severing the connections between crypto and the real economy.

One of the greatest appeals of cryptocurrency, at least to crypto touts, is the potential to replace state-issued currency with decentralized and autonomous alternatives. The theory goes that this replacement will lead to greater transparency, freedom, and equality by separating the power of the state from money.

Despite this lofty goal, to date the crypto-conomy remains dependent on “fiat” currency to do business. It turns out that it is still pretty difficult to pay bills using blockchain tokens. This means that cryptocurrency traders like having the ability to convert crypto into dollars, euros, and other state-backed money. At the same time, crypto businesses need continued inflows of real money to keep their operations running.

Unfortunately for the crypto exchanges, the collapse of the FTX fraud has forced regulators to start taking a much closer look at how these entities do business. Due to their penchant for convoluted offshore structures, questionable ownership, and propensity to get involved in dirty business, there is increasing pressure on traditional banks to stop doing business with crypto businesses. Recent news demonstrates that the pressure is increasing, with the consequence that the crypto-conomy is being isolated from the real world of finance.

Let’s take a look.

Binance cut off from US banking

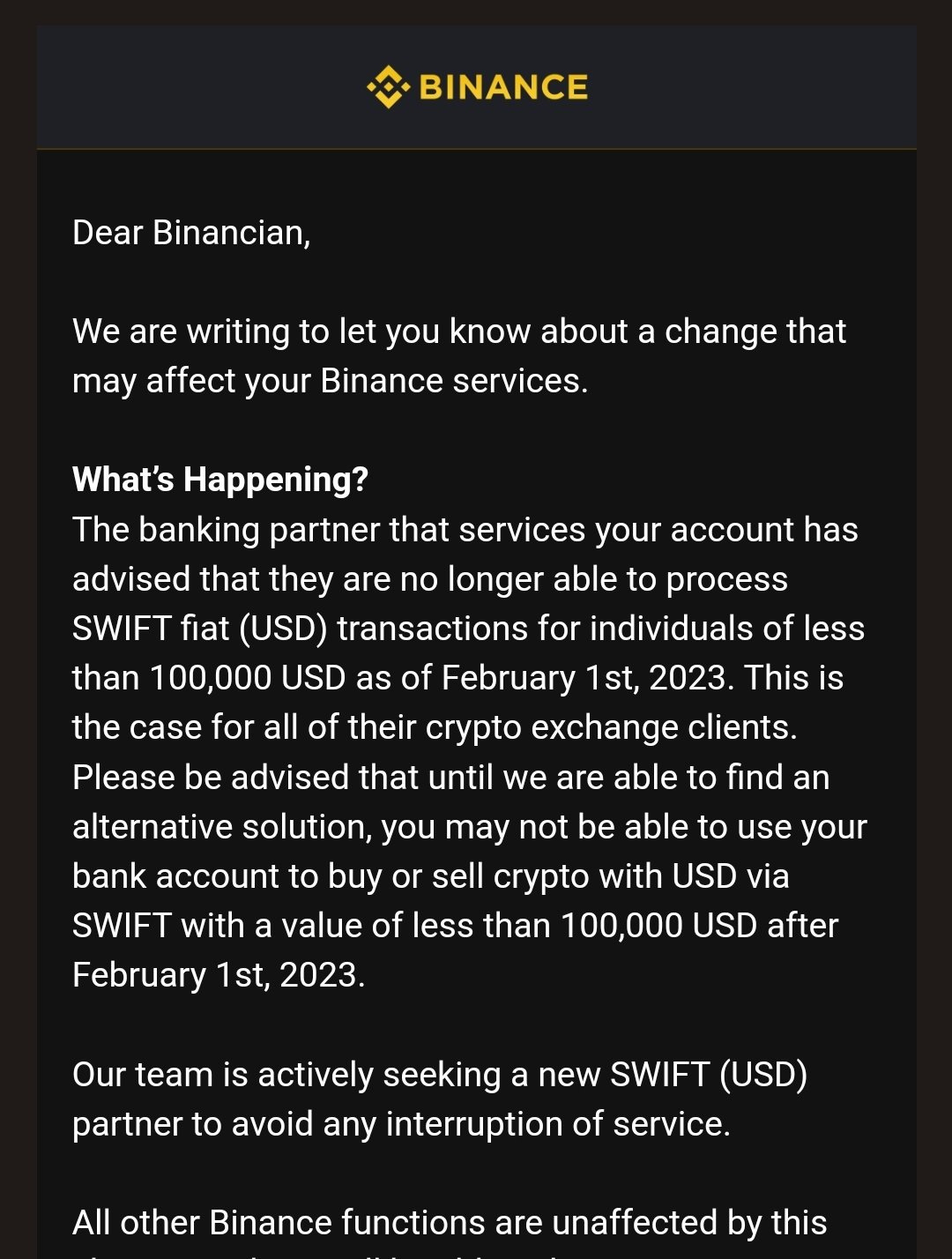

On January 21st, Binance customers received an email stating that starting February 1st, the exchange would no longer be able to process dollar transfers over SWIFT of less than $100,000. According to this notice:

The banking partner that services your account has advised they are no longer able to process SWIFT fiat (USD) transactions for individuals of less than 100,000 USD as of February 1st, 2023. This is the case for all of their crypto exchange clients. Please be advised that until we are able to find an alternative solution, you may not be able to use your bank account to buy or sell crypto with USD… Our team is actively seeking a new SWIFT (USD) partner to avoid any interruption of service.

As we had previously reported, Binance was using Signature Bank of New York to process dollar transfers via a Seychelles shell corporation, Key Vision Development LTD. A few hours after Binance’s new USD limits became public, Bloomberg confirmed that Signature Bank was Binance’s banking partner and had placed these new limits on their activity.

We find it interesting that Signature chose to place these onerous limits on Binance just days after we and others publicized their questionable relationship!

Things just got worse from here: Yesterday, Binance notified its customers that ALL dollar transfers would be suspended in just two days:

This means that, effectively, Binance customers are unable to directly transfer US dollars into, or out of, the exchange. Binance customers are now being directed to use their “peer to peer” service, where individuals sell crypto for dollars directly in a marketplace faciliated by Binance. This seems like a good alternative to a normal bank transfer, except for the part where your “peer” steals your money:

Of course, this is just a “temporary” issue because Binance won’t have any problems finding a new U.S. bank to do business with.

Right?

Crypto.com’s payment processor shut down by Lithuanian authorities as part of massive fraud crackdown

Crypto.com, of Matt Damon and Staples Center fame, had been processing Euro transfers through a company called Transactive Systems. Transactive is a Lithuanian payment processor owned by a British corporation called Transactive Systems Ltd. Transactive’s CEO and director was previously the “country director” for a major payments firm called Payoneer. Notably, Payoneer had its own issues with providing services to fraudulent entities.

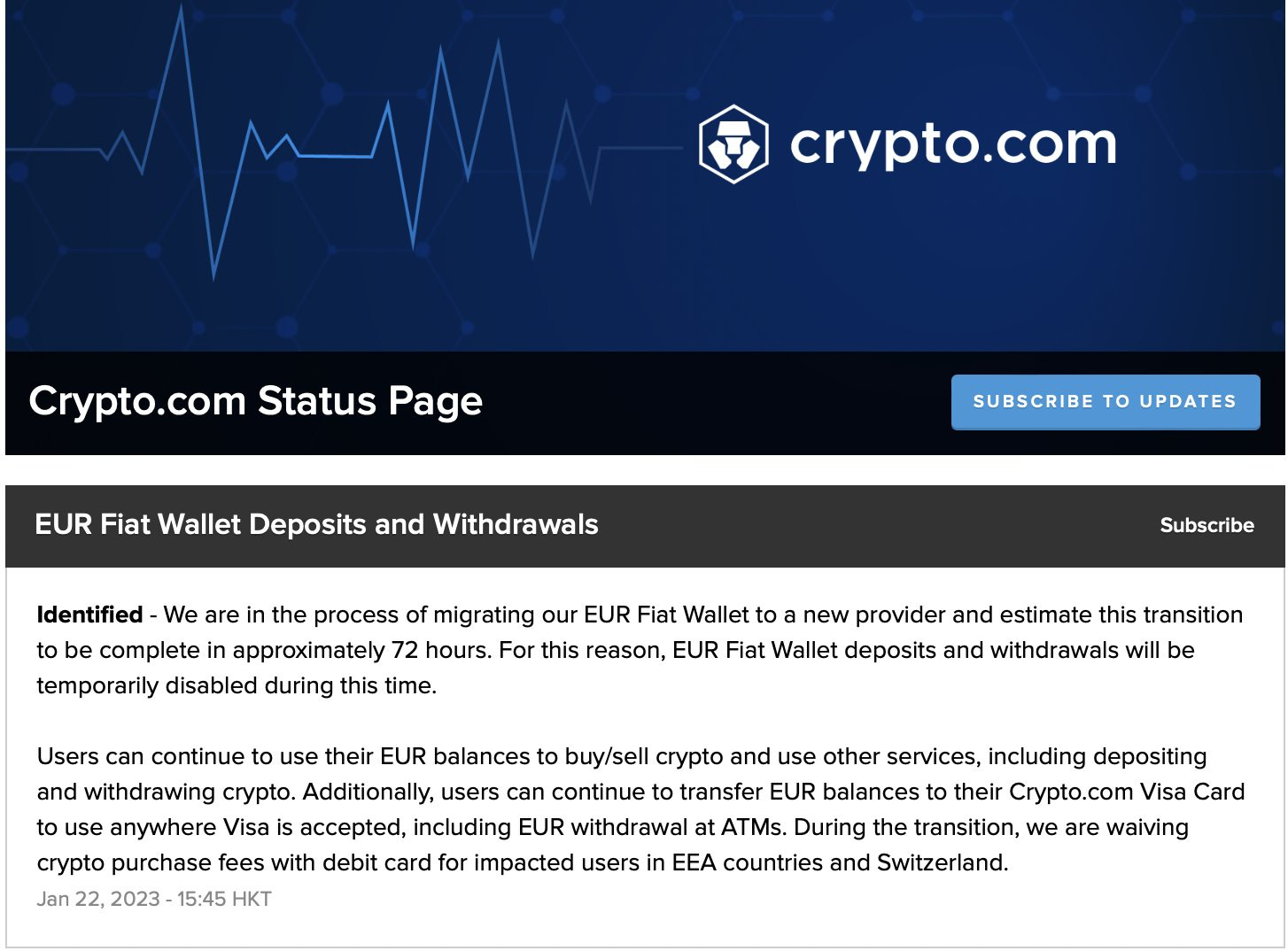

On January 22, Crypto.com users began reporting that they were unable to make or receive Euro transfers. Shortly thereafter, Crypto.com announced that they were “migrating” to a new payment processor:

Tracking down the reasons for this switch, a sharp-eyed crypto researcher discovered that Transactive’s website had an interesting new notice:

It turned out that Lithuanian authorities had essentially shut Transactive down for flagrant violations of money laundering and international sanctions. Notably, another crypto client of Transactive was Nexo, which was recently raided as part of an international investigation into fraud and possible sanctions violations…

Bloomberg subsequently published a detailed report about Transactive, including more interesting history about some of its employees:

Multiple high-level employees who helped set up and run Transactive came from PacNet Services Ltd., a company that had to close down after being sanctioned by the United States for being the “payment processor of choice” for scam artists. Several are being targeted by authorities, including one facing federal fraud charges who remained a senior Transactive employee until just weeks ago. In June, a founding investor was sentenced to two years in jail for his part in an unrelated $1 billion healthcare fraud.

According to Bloomberg, Transactive was moving tens of billions of euros annually before the crackdown and was the second-largest electronic money processor in Lithuania.

Crypto.com eventually resumed transfers, now using a Malta-based payments processor called OpenPayd. OpenPayd also acts as payment processor for the infamous Bitfinex exchange, demonstrating this firm’s willingness to do business with literally anyone….

What’s coming next?

Regulators and enforcement agents are now circling the crypto industry. In the wake of the collapses of FTX and Genesis, the pressure on anyone doing business with crypto entities will continue to grow. With key crypto servicing banks like Signature and Silvergate deserting the industry, these firms and their customers will face increasing challenges getting their hands on “fiat” currency.

We will continue to focus on the methods being used to move real money into the crypto-conomy in the coming days. These investigations might lead to some interesting places. Stay tuned.

I love your work

People who let their instincts tell them to stay away from the crypto business way back when it started...just after the big bubble burst - knew the fact it was so obscure meant simply that it was a set up to allow fraud & theft financial deals to be hidden, and any fancy explanations made no sense whatsoever apart from that one. I also assumed that just like any other fancy illegal business it would have a few years of glory & then collapse on itself spectacularly - and here we are !!! Those who think they are running a legal crypto business are just kidding themselves - the whole point of it's invention was to stay out of the view of financial inspectors - for what reason could that possibly be ?