Is Nexo Nexto?

According to state regulators, the crypto lending firm is insolvent without their $NEXO token holdings. The same situation that led to Celsius Network's collapse...

On September 26, 2022, eight states filed emergency cease and desist orders against the crypto lending firm Nexo. The regulators assert that Nexo has been offering various products illegally to state residents and that the company has misrepresented the risk associated with those products. The regulators also make a shocking claim: The only asset standing between Nexo and insolvency is their propietary token, $NEXO.

At this point, anyone familiar with the failure of Celsius Network will sit up in their seats.

Nexo Targeted by State Regulators

Founded in Bulgaria, the crypto community considers it one of the most financially responsible crypto lending firms. Indeed, it is practically the “last man standing” after the collapse of Celsius Network, the bailout of Blockfi, and the failures of many smaller centralized lending platforms like Hodlnaut. Nexo has even made public statements suggesting that they might buy the remnants of Celsius to restore liquidity for investors:

Nexo bills itself as the digital asset equivalent of a bank, except better. You can use crypto assets as collateral to borrow “fiat” currency at relatively low interest rates from Nexo. They also offered an “Earn” product, similar to a savings account, where you can make deposits of crypto assets and receive yield. However, in February of this year Nexo announced that they would no longer offer Earn products to new U.S. users due to concerns about U.S. securities violations. This happened after the SEC “provided clarity” on the question of crypto lending by fining Blockfi $100 million for offering unregistered “earn” products.

In the new cease-and-desist (“C&D”) orders issued against Nexo, the various states allege that Nexo offered a variety of financial securities without registering them or providing critical information about these products to investors. According to the C&D order from Kentucky regulators, Nexo failed to even register to do business in the state of Kentucky. The C&D states that Nexo is a conglomerate of several entities, which primarily do business through Nexo Capital, Inc., a Cayman Islands-based corporation.

The Kentucky C&D contains a critical assertion, based on an investigation by the state regulators:

As of July 31, 2022, Nexo Capital (which conducts the business of Nexo on its website and move application) held 959,089,286 in NEXO tokens, comprising 95.9% of all tokens in existence, and valued those tokens at $682,823,570.

Excluding Nexo Capital’s net position in NEXO, Nexo Capital’s liabilities would exceed its assets.

This is a big, big, big problem… because a very basic market analysis demonstrates that Nexo would be unable to monetize a significant chunk of these tokens. Given that fact, the true value of the $NEXO tokens on Nexo’s balance sheet is likely close to $0.

Another illiquid token marked-to-market

Like Celsius Network, Nexo created its own Ethereum token, $NEXO, and sold these tokens as part of an “Initial Coin Offering” in 2018. Per the Kentucky filing, Nexo sold 525 million tokens during the ICO, retaining the remaining 475 million $NEXO on its own balance sheet. Nexo could then mark-to-market their $NEXO holdings and show good financial health.

According to regulators, Nexo now holds ~95% of the total NEXO tokens in existence on its balance sheet. A quick glance at the token distribution on Etherscan bears this claim out, as the major addresses holding $NEXO are directly linked back to the company:

Again, this is nearly identical to the situation of Celsius Network. Celsius ended up directly owning approximately half of the $CEL tokens in existence. Deposits and collateral from customers also ended up under Celsius control, leaving Celsius holding over 90% of the total tokens in existence. This created a massive imbalance between the concentration of $CEL tokens and the liquidity available in markets for $CEL token, making it impossible for Celsius to use their $CEL to patch holes in their leaking financial statements.

NEXO token is in the same situation, as its markets are highly illiquid. On 9/26/22, for example, the total trading volume for $NEXO token across all markets curated by CoinGecko was $8.4 million, equivalent to <1% of the total market cap of $NEXO. In fact, NEXO token is even more illiquid than the bankrupt Celsius Network’s CEL token.

$NEXO’s true trading volumes may be much lower

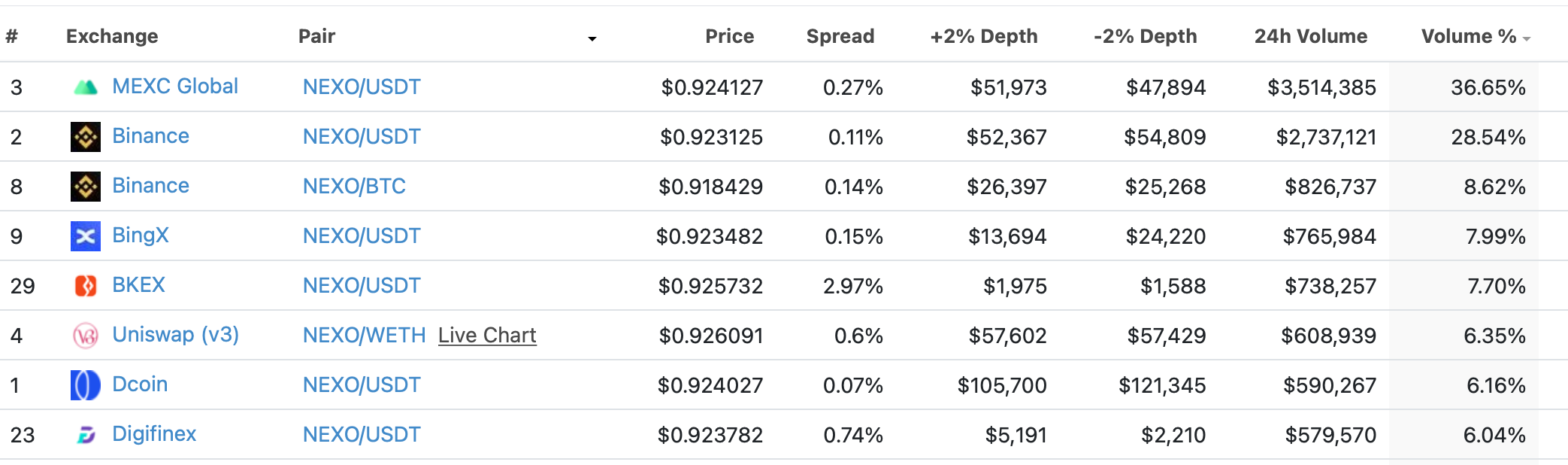

There are several red flags that suggest $NEXO trading volumes may be even lower than suggested by market aggregators. The highly questionable MEXC Global exchange claims to host the largest trading pair for $NEXO. We have previously shown that MEXC has multiple ties to a network of fraudulent crypto exchanges registered by a shady Colorado firm:

Oddly enough, when we looked at MEXC Global’s official Ethereum wallet, we discovered that it only holds 95,716 $NEXO tokens, despite hosting several millions of dollars worth of daily NEXO trades. In other words, MEXC Global’s daily NEXO trading volumes are roughly 40x higher than the total number of NEXO tokens they hold in their main wallet:

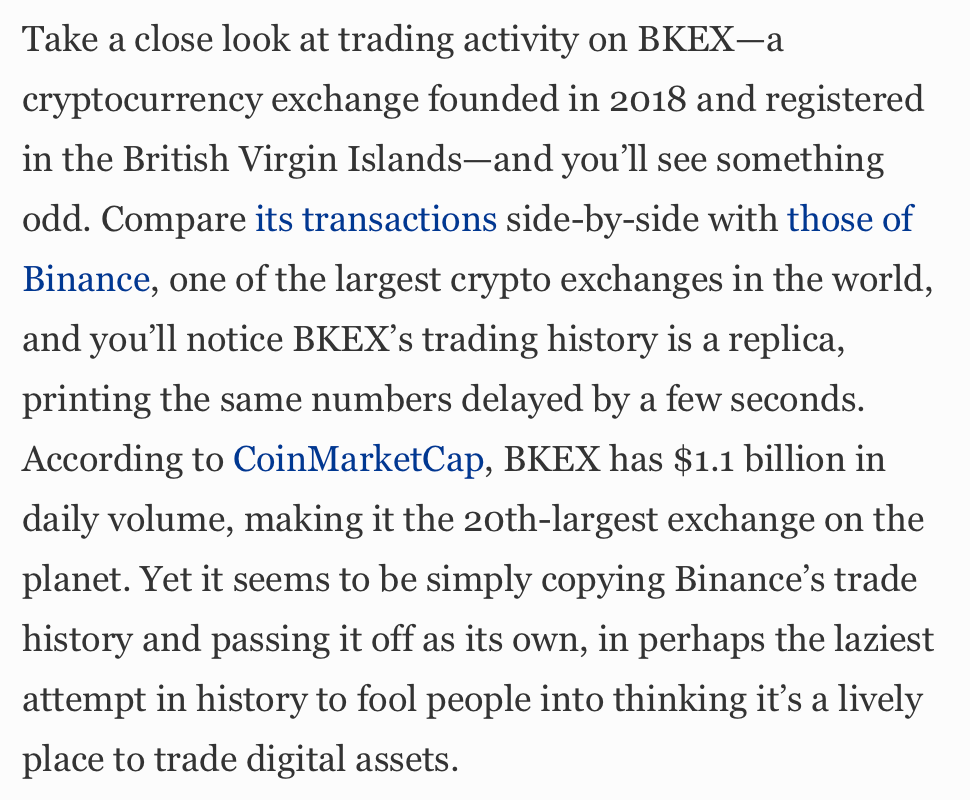

Another 7% of $NEXO trading volume was attributed to the BKEX Exchange. Oddly enough, there is a Forbes article from 2019 about BKEX producing fake crypto trading volume:

Not to malign the BingX exchange (also home to roughly 7% of $NEXO), but I’ve never heard of it. Same goes for “DCoin,” hosting about 6% of daily volume. And we have previously shown how inflated trading volumes are on decentralized exchanges like Uniswap.

While not conclusive, this data suggests that a significant percentage of NEXO’s already anemic trading volume may be fake. This would only exacerbate the already horrible liquidity problem NEXO faces should they try to liquidate even a small fraction of their total holdings.

Conclusion: The Flywheel Model, Redux

It is impossible, given current market conditions, that Nexo could ever sell a significant fraction of their tokens without crashing the $NEXO market. Also, our data suggests that a significant fraction of $NEXO trading volume might not be legitimate.

Consequently, the real value of the tokens on their balance sheet should be marked down to near $0. Like Alex Mashinsky’s “flywheel” model, Nexo apparently tried to use their token to spin up hundreds of millions of dollars in free assets. This strategy works… until it doesn’t. So, if Kentucky regulators are correct and that all that stands between Nexo and insolvency is their token…

Good luck!

man like nexo token is basically an exchange token. of course everyone's gonna hold it on nexo cause its the only place it has utilities -- what use you have of it holding it on a ledger?! so naturally everuyone holds nexo on... nexo.. shocker. look at all the other exchange tokens, same shit with FTX etc.

lots of words in this article instead of a simple explanation.

Nice work. We will study it and inform our Spanish speaking community, integrating back links to the article and your site. Kind regards.