Mashinsky's Flywheel

How the CEL token built, and destroyed, the Celsius Network

Charles Ponzi arbitraged “international reply coupons” to make his investors rich. Allen Stanford sold certificates of deposit that were safer than the Federal Reserve. Bernie Madoff generated above-market returns with genius options trades.

And Alex Mashinsky had his flywheel.

Over the last few months, I’ve spent a lot of time examining how Celsius Network operated. In particular, I ended up spending far more time than I ever intended learning about the firm’s propietary cryptocurrency, CEL token. Despite CEL being a rather obscure cryptocurrency, it turned out that the token was essential for understanding how Celsius worked.

Now, it appears that securities regulators are examining CEL token as well. Today, the Vermont Department of Financial Regulation filed a motion in Celsius Network’s Chapter 11 case encouraging the appointment of a bankruptcy examiner. As part of this filing, the regulators pull no punches and assert that:

Celsius also admitted at the 341 meeting that the company had never earned enough revenue to support the yields being paid to investors. This shows a high level of financial mismanagement and also suggests that at least at some points in time, yields to existing investors were probably being paid with the assets of new investors.

If this claim is true, this means that Celsius Network meets the definition of a Ponzi scheme. The regulators appear to believe that the CEL token was a central part of this scheme, stating that:

Credible claims have been asserted publicly, through letters to this Court and otherwise, that Celsius and its management engaged in the improper manipulation of the price of the CEL token, including by using the proceeds of investor deposits to acquire CEL tokens and increase its Net Position in CEL.

The regulators conclude that:

17. …By increasing its Net Position in CEL, Celsius invested depositor assets in a long position in CEL that was inconsistent with its purported “market neutral” investment strategy.

18. During the 341 meeting, Celsius admitted, through its CFO Chris Ferraro, that the decline in the price of CEL contributed to its insolvency.

19. An Examiner should investigate whether Celsius improperly deployed assets to manipulate the market price of CEL, thereby artificially inflating the value of the company’s net position in CEL on its balance sheet and financial statements.

20. An Examiner should investigate whether or not the company’s actions and practices improperly enriched Celsius insiders and other holders of CEL tokens at the expense of retail investors in Earn accounts.

Of course, readers of this blog and our Twitter account (which has recently been re-instated!) had heard most of these allegations months ago:

Today, let’s look at how CEL token, the “backbone of the Celsius Network” ended up destroying Celsius Network.

How CEL was supposed to work

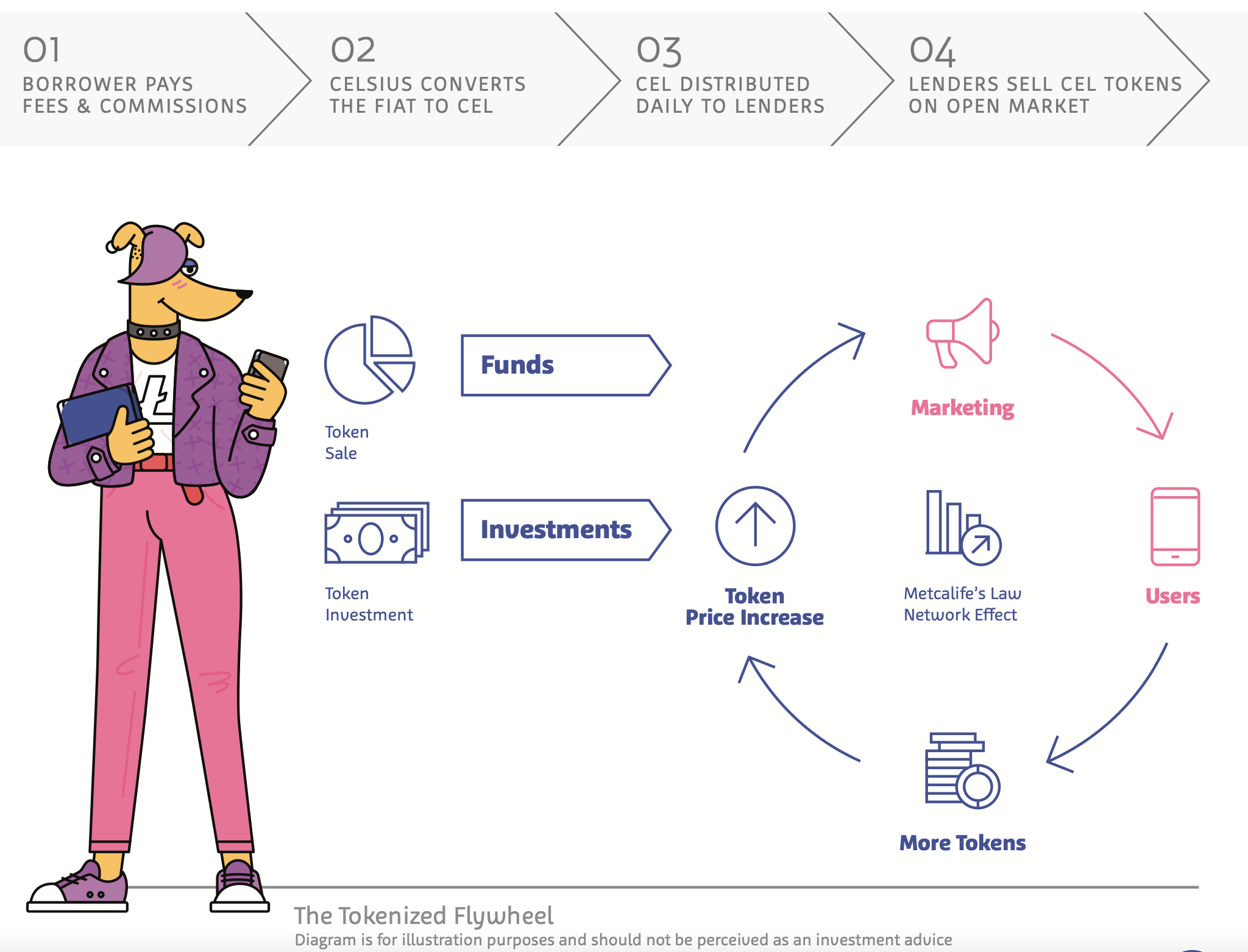

At the inception of Celsius Network, the CEL token was described as “the backbone” of their innovative financial system. Customers would deposit their other crypto assets, like Bitcoin or Ether, and then be paid yield back in the form of CEL tokens. The company would buy CEL tokens on the market using their profits, driving up the price of the tokens. This would create what Alex Mashinsky referred to as the “Celsius Flywheel:” As the company made more returns, the price of CEL would increase:

According to the Celsius Network white paper:

We’re designing CEL token to be the backbone of the Celsius Network, creating a value-driven lending and borrowing platform for all our members

And, for a while, it seemed that the model was working. CEL token, initially sold for $0.30 to the general public, quickly rose in value. In early June of 2021, it hit its all-time high of $8.05:

It is thus very interesting that the Vermont regulators zoom in on the period between May and December 2021. According to their filing, Celsius financial records show that:

From May 24, 2021 to December 14, 2021, Celsius increased its Net Position in CEL by 41,955,119 CEL tokens, when the market price of CEL generally ranged between $3.86 and $8.00. Declaration of Ethan McLaughlin at ¶ 6f.

In theory, the funds used to make these CEL token purchases should have come from the profits generated by Celsius’ various yield-generating strategies. In theory…

Where did the money come from?

Based on court filings and our own investigations, it appears that Celsius may have directly spent customer deposits to drive up the price of CEL token. In July 2022, a former Celsius Network employee named Jason Stone sued Celsius in New York state court alleging that Celsius owned his firm KeyFi, Inc. millions of dollars related to services he provided during his relationship with the firm. In this filing, Stone alleged that Celsius had committed fraud to increase the price of CEL token:

Connor Nolan, head of coin deployment at Celsius, informed Stone that Celsius had used approximately 4,500 Bitcoin, with a current value of $90 million, in customer deposits to purchase CEL on the open market between February 2020 and November 2020 to artificially inflate the price.

Essentially, these transactions made Celsius Network short Bitcoin, at a time when Bitcoin’s price was rising dramatically. Simultaneously, the company was massively increasing their long position on CEL token, meaning that a decline in the value of CEL would adversely impact the company’s finances.

The claims by Mr. Stone appear vindicated by today’s filing, which asserts that Celsius Network admitted the firm had “never earned enough revenue to support the yields being paid to investors.” If this is true, Celsius would have had to use customer deposits or loan collateral to purchase CEL token on the market.

We know for a fact that Celsius was buying CEL on the market due to Alex Mashinsky, who on multiple occasions asserted that Celsius was the largest buyer of CEL token in the market.

Why did Celsius choose to take this approach? I believe there were two reasons: First, to inflate the value of the company. Second, insiders like Alex Mashinsky ended up realizing millions of dollars in profit from their CEL token holdings.

CEL Token was Celsius Network

Since its inception, the largest holder of CEL token was Celsius Network itself. The company retained 117 million tokens, approximately 1/6 of the total tokens, on its balance sheet in a “treasury.” Per the company, these tokens were never to be sold. In addition, Celsius owned millions more CEL tokens and increased the amount owned over time. As of its bankruptcy, it appears Celsius owns some 379 million CEL in total.

Since Celsius Network was the largest buyer of CEL token and controlled the price of the token, it seemed incredible that the firm included its CEL token holdings on its balance sheet:

By including CEL token on its balance sheet, Celsius Network was able to massively inflate the value of the company. As pointed out by the excellent investigator @intel_jakal, it would have been impossible for the company to sell these tokens at anywhere near market price:

If these allegations are true, the “Celsius Flywheel” worked more like this: Celsius customers deposited funds, assuming those funds would be used for lending or DeFi applications to earn yield. Instead, Celsius used those funds to purchase CEL tokens and maintain or increase the price of the token. Then, Celsius could go to investors like Westcap and the CDPQ and show a nice, healthy balance sheet bulked up by CEL token. Celsius could spin up billions of dollars in assets with this neat trick!

Insiders Cashing Out

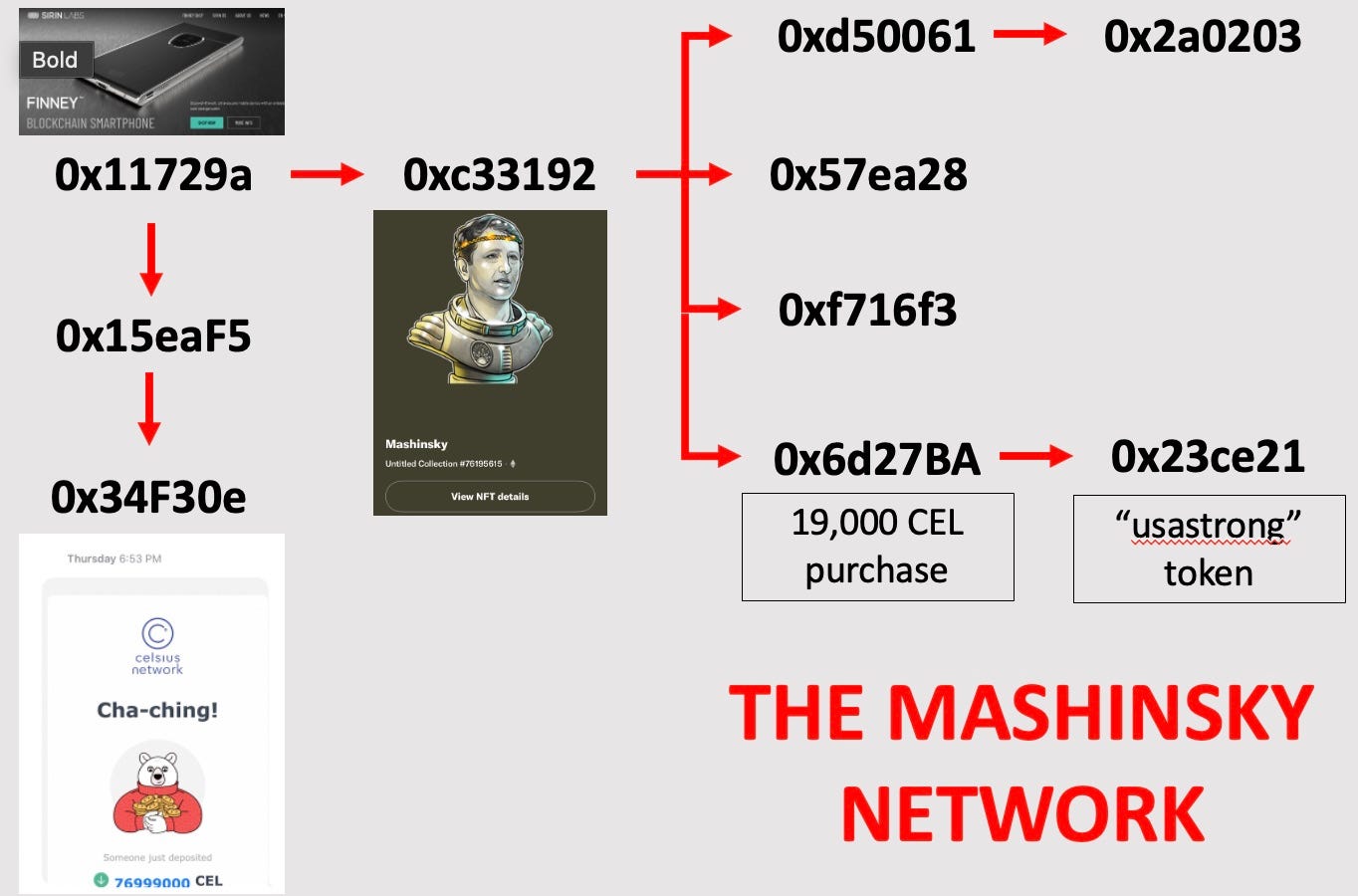

Of course, there was another benefit to pumping CEL token price and liquidity: It enabled insiders like Alex Mashinsky to cash out, big time. As we have showed conclusively, wallets linked directly to Mashinsky sold tens of millions of dollars worth of CEL token over the last couple of years:

Mashinsky preferred to use decentralized exchanges (DEXs) like Uniswap for this purpose. Incidentally, we demonstrated that >60% of the liquidity on these DEXs were attributable to the market making firm Wintermute. Conveniently, while responding to the allegations in this article, the CEO of Wintermute casually volunteered that Wintermute had a “relationship with Celsius” to provide liquidity in these markets:

So, we can prove that Celsius employed a market-making firm to supply liquidity to the very markets that their CEO was selling on!

In addition, a recent article in the Financial Times (which has provided excellent coverage of the Celsius Network saga) asserted that corporate leadership sold over $40 million of CEL tokens directly back to the company. This included co-founder and Chief Strategy officer S. Daniel Leon:

While the company was buying, top executives were selling. On the same day Leon posted his video touting the future of crypto, Celsius trading records show that he sold $1.8mn of CEL back to the company — one of 16 disposals of CEL by Leon to Celsiusbetween October 2020 and August 2021 that generated $11.5mn in total. Leon did not respond to requests for comment.

And co-founder and former CTO Nuke Goldstein:

Nuke Goldstein, a Celsius co-founder who calls himself "el presidente of innovation", sold $4.1mn worth of CEL between November 2020 and May 2021. In an email response to the FT, Goldstein said he was seeking permission to comment from Celsius. In May, he tweeted "my [CEL] rewards created an enormous tax liability (reported as income) and I was selling some to cover and hedge", adding that he saw "no logic" in claims that Celsius's founders were selling CEL to line their pockets.

It is plausible that there are more sales by insiders that have not been revealed. Celsius had a habit of making large transfers of CEL token directly to exchanges like FTX, making it difficult to ascertain exactly who was buying or selling at any given time. In August of 2019, Alex Mashinsky tweeted that he had just deposited 77 million CEL tokens (~11% of total market cap) into Celsius:

According to Celsius’ “Top 500 HODLer” list, a list of the biggest holders of CEL token in Celsius, Mashinsky now “HODLs” about 50 million CEL under his nickname, “The Machine.” If this represents the totality of his CEL holdings, there are several million CEL unaccounted for in our prior analysis…

The Final Days of Celsius

The flywheel was spinning… until it stopped.

Celsius began facing increasing liquidity pressures due to crypto market changes. In early May 2022, the Terra Ponzi scam collapsed. It was discovered (in part due to our investigations) that Celsius had been investing large sums into the Terra scheme. Celsius was able to pull out in time and only experienced small losses, but investors began to lose confidence in both their management and the wider crypto markets. When we reported on their massive staking of Ether in the ETH2 contract, limiting their liquidity, this also led to some concerns about liquidity.

At the same time, CEL token price collapsed in value. Celsius had pulled the plug, likely because they could no longer afford to cover the costs of supporting the price. Customers who had borrowed using CEL token as collateral were liquidated in droves, turning sentiment against the company.

And as CEL token plummeted, so did Celsius’ value as a business. Mashinsky’s Flywheel starting spinning in the opposite direction, shredding the company’s balance sheet. By early June, it was clear the company was under major stress. Now insolvent even by the most generous assessments, the company could not attract new investors.

Since the company had spent customer deposits to support CEL token, the loss in value cut even deeper. The firm didn’t have the assets they owed and they didn’t have anything to show for it.

And on June 12th, the flywheel stopped spinning.

I hate to say I told you so, but…

Your number of CEL in the treasury was much lower than I believe Celsius said they had in there. Thanks for the research.