One of these stablecoins is not like the others...

A look at the reserves backing the three largest stablecoins in the crypto-conomy.

Have you ever been in an arcade? To play the games hosted inside the arcade, you must first exchange your money for arcade tokens. These tokens act as dollar equivalents within the micro-economy of the arcade. At the end of your sojourn within the fantasyland of the arcade, you can (sometimes) sell your tokens back in exchange for real money.

Stablecoins are the crypto equivalent of an arcade token. In its simplest form, the stablecoin issuer accepts one unit of currency in exchange for a blockchain entry equal to that unit of currency. So, $1 is equivalent to 1 $USDC or 1 $USDT. Entities can then use these dollar equivalents to purchase other cryptocurrency directly on the blockchain or execute other trades, loans, transfers, etc.

In exchange for creating a blockchain-usable dollar equivalent, the stablecoin issuer gets to hold the real dollars and collect any interest earned on these assets. However, the issuer explicitly promises to hold all of these assets in safe and liquid assets to ensure that the value of their reserves always equals the value of the stablecoins they have issued. In other words, an stablecoin issuer should function like a simple money market fund.

There are three large stablecoins in the cryptocurrency market with a collective marketcap of $130 billion dollars. This is roughly 14% of the total cryptocurrency market cap. Together, these three stablecoins make up >99% of the liquidity within cryptocurrency markets.

Of these stablecoins, the Tether stablecoin is the largest with a current market capitalization of $65 billion, followed by Circle ($43 billion) and BUSD ($22 billion). By daily trading volume, Tether also (usually) dominates the market. Other than a brief period during the FTX failure when BUSD volume skyrocketed (???), Tether’s volume typically outpaces the other two stablecoins by several fold:

In other words, Tether serves as the primary source of dollar liquidity in cryptocurrency markets.

This raises an important question: What assets are backing these stablecoins? And is it possible that one of these stablecoins is not fully backed?

What’s backing each stablecoin?

USD Coin ($USDC):

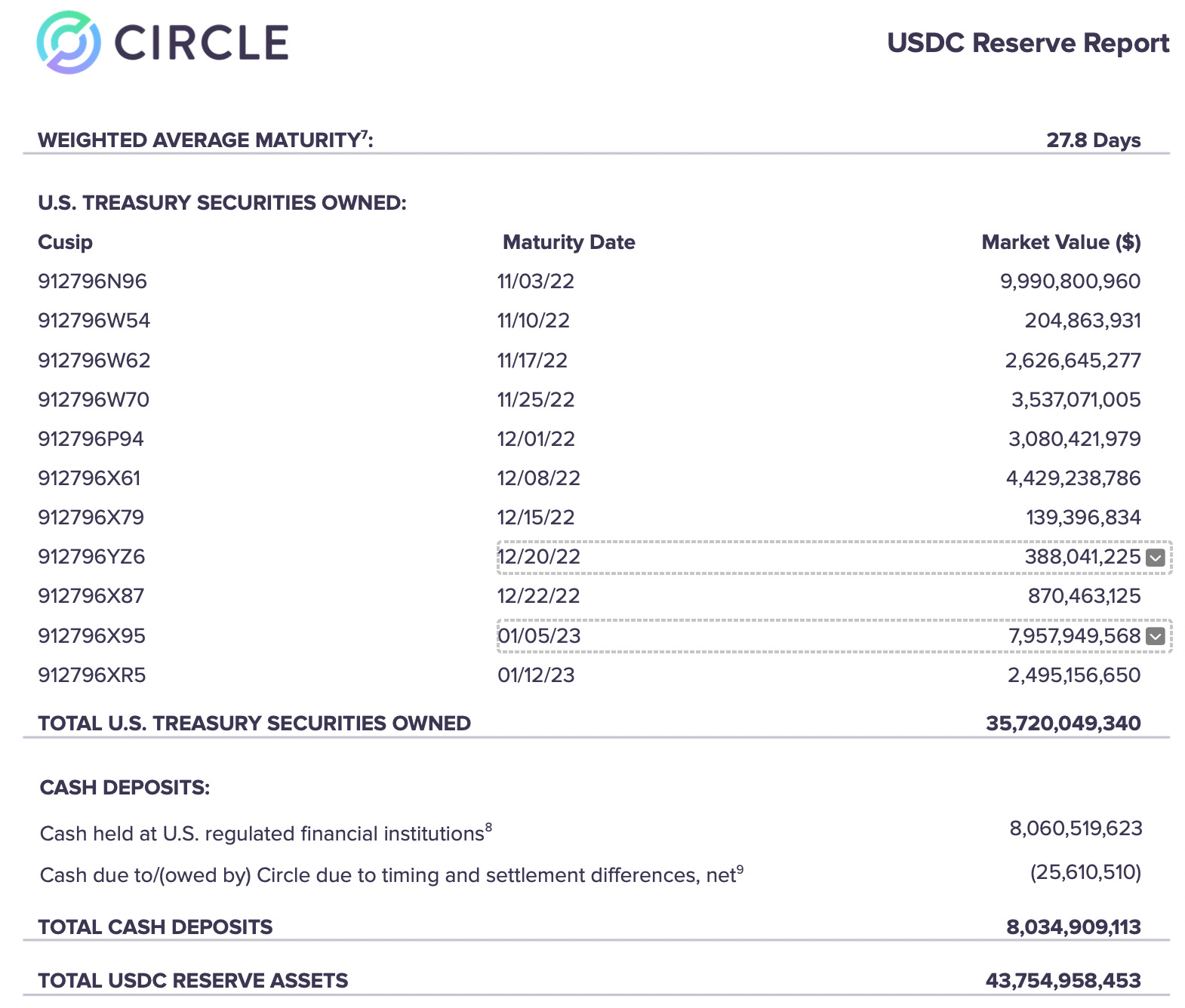

USDC is issued by Circle Internet Financial, LLC, a U.S. based company licensed as a money transmitter. USDC has a current market capitalization of $43 billion. While Circle has never published an audited financial report, they do provide monthly “attestations” from their accounting firm, Grant Thorton. The most recent report, for October 31, 2022, shows that USDC is fully reserved primarily with Treasury securities (82%) and cash (18%). Circle asserts that all of their cash is held at “U.S.-regulated financial institutions:”

Note that the USDC attestation provides the Committee on Uniform Securities Identification Procedures number for each issue of Treasury securities purchased, along with the market value of each.

Despite the caveat that these statements are unaudited, Circle’s disclosure provides a fairly good level of detail about the assets backing their reserves. They hold a relatively simple mix of liquid and low-risk assets that would be easy to liquidate in case holders of their stablecoin wanted to redeem their dollars.

Binance USD ($BUSD):

While Binance USD has the name of the world’s largest exchange, the stablecoin is actually issued by the Paxos Trust Company, LLC, a New York-based financial firm primarily working with cryptocurrency. Paxos holds the reserves underlying BUSD, which currently has a market capitalization of $22 billion. Like USDC, Paxos issues unaudited monthly reports describing the reserve breakdown:

Based on their attestation from October 2022, BUSD was backed with a combination of US Treasury debt ($6.1 billion or 29% of market cap), Treasury Reverse Repurchase Agreements ($14.2 billion or 67% of market cap), and cash ($870 million or 4% of market cap).

Like USDC, Paxos reports that the cash portion of the funds are held at U.S. regulated banks. Again, the BUSD reports provide substantial detail about the reserves backing the stablecoin. And, like USDC, the composition of the stablecoin’s reserves is simple and composed entirely of low-risk assets.

Tether ($USDT):

The Tether stablecoin is both the oldest and largest stablecoin in the market. It is owned by the same folks that run the Bitfinex exchange, although ostensibly Tether and Bitfinex are separate entities. As we will show, the separation between these two firms is similar to the supposed separation between the FTX exchange and Alameda Research.

Unlike Circle and Paxos, which are both licensed to operate in the state of New York, Tether is specifically banned from doing business in New York. Tether had to pay $18 million in a settlement with the NY AG after it was proven that they had lied about the reserves backing USDT. It turns out that at several points throughout Tether’s history, their advertised 1:1 backing with U.S. dollars was a lie. Furthermore, Tether and Bitfinex frequently commingled assets, sharing funds to prevent insolvency.

Anyway, let’s forget about that totally irrelevant past and take a look at Tether’s most recent attestation, for September 30, 2022:

Gee, that sure looks a lot different from the financials released by Circle and Paxos, doesn’t it? Treasury bills and cash make up 67% of their reserves. Another $7.1 billion (10.3%) of the reserves are held in money market funds. Tether does not disclose the breakdown of which Treasury debt it owns or where they do their banking.

Notably, $11.9 billion (18%) of these reserves are attributed to “other investments,” “secured loans,” and “corporate bonds, funds, and precious metals.” Another $3 billion (4.4%) are held in “reverse repurchase agreements.” Unlike the reverse repo agreements listed on BUSD’s balance sheet, these are not Treasury-backed assets. Instead, these are:

agreements that have been entered into directly or indirectly by means of the purchase of structured notes or fund vehicles, where the ultimate issuer or guarantor of the agreement has a rating of A-2 or better.

Who are these secured loans to? We don’t know, because Tether doesn’t tell us. We know that at least one former creditor was the Celsius Network, which Tether ended up liquidating for >$900 million in June of 2022.

What are these loans secured with? We don’t know, because Tether doesn’t tell us. Based on their deal with Celsius, we know that Tether issued USDT based on Bitcoin-backed loans.

What assets make up Tether’s $2.6 billion in “other assets?” We don’t know, because Tether doesn’t tell us. A recent report from Semafor claims that some of these assets are venture capital investments Tether made in (likely worthless) companies:

It also owns $2.6 billion in “other investments,” according to the September report. It’s not totally clear what’s in them, but they are likely venture stakes in other crypto companies held by its owners and affiliates, according to a global investigations firm commissioned by a hedge fund betting against the price of Tether. Semafor reviewed the findings of its report that found Tether holds equity stakes in more than a dozen crypto startups.

Semafor was able to verify some but not others. We confirmed that the crypto exchange that owns Tether invested, either through itself or an affiliate, into: an online-betting site called Betfinex; Dazaar, a data-sharing service; Dusk Networks, whose software turns financial investments into tokens; a crypto trading platform called Rhino; Shape Shift, a crypto wallet; Blockstream, a blockchain infrastructure company; Netki, a digital-ID company; and Keet.io, a video-chat app.

Obviously, Tether’s disclosures and reserves strategy differs wildly from its major competitors. Their attestations don’t show anywhere near the same level of detail as either Circle or Paxos. Their strategy is far more complex and Tether admits to holding more risky assets on the balance sheet. And, it appears that at least some of Tether’s reserves are held in highly illiquid venture capital investments that may be worth significantly less than what Tether claims they are.

…wait, Tether admitted to lying about their reserves?

In 2021, Tether settled lawsuits by the New York state Attorney General (NYAG) and the Commodities and Futures Trading Commission (CFTC), paying $18 million and $41 million in fines respectively. In those settlements, it was proven that Tether had lied about the assets backing their token on multiple occasions. In fact, these settlements demonstrated that Tether was fully backed about 28% of the days over a several-year period. Per the NYAG statement about the settlement:

The OAG’s investigation found that, starting no later than mid-2017, Tether had no access to banking, anywhere in the world, and so for periods of time held no reserves to back tethers in circulation at the rate of one dollar for every tether, contrary to its representations.

One particularly egregious event disclosed in these settlements was in 2018. The Bitfinex exchange was using a Panama-based shadow bank called Crypto Capital Corp (CCC) to handle its funds. Notably, the deal between CCC and Tether did not include any written contract. Unfortuantely for Tether, CCC happened to also be doing business with the cartels. It was shut down by the U.S. DOJ and their assets were seized, including some $850 million in Bitfinex customer funds. To cover up the losses, Bitfinex moved Tether’s reserves to its own accounts:

On November 1, 2018, Tether publicized another self-proclaimed ‘verification’ of its cash reserve; this time at Deltec Bank & Trust Ltd. of the Bahamas. The announcement linked to a letter dated November 1, 2018, which stated that tethers were fully backed by cash, at one dollar for every one tether. However, the very next day, on November 2, 2018, Tether began to transfer funds out of its account, ultimately moving hundreds of millions of dollars from Tether’s bank accounts to Bitfinex’s accounts. And so, as of November 2, 2018 — one day after their latest ‘verification’ — tethers were again no longer backed one-to-one by U.S. dollars in a Tether bank account.

Of course, this was the past. Although Tether and Bitfinex are still controlled by the same individuals, maybe they turned over a new leaf?

Perhaps not. Because, even if we take Tether’s current attestations at face value, their own numbers demonstrate that Tether has either been insolvent multiple times over the past year, or they have required recapitalization on multiple occasions!

As the inimitable software consultant and financial writer Patrick McKenzie explains:

The Consolidated Reserves Report alleges that Tether’s reserves included, as of September, $2,617,267,750 of “Other Investments (including digital tokens)” and $6,135,946,415 of Secured Loans.

These assets must have been impaired in the last six weeks. If they are not, Tether would have a legitimate claim to being the best risk managers. Not in crypto, no, in the history of the human race.

The risk-on assets are 12.86% of the reserves, via simple division. Their equity is 0.36% of assets. (No, I did not forget to multiply by a hundred when converting to percent.)

If their risk-on assets were impaired by more than about 2.86%, Tether must have (by their own numbers) needed recapitalization. Again.

Despite issuing loans to other crypto firms, Tether has somehow avoided losses on every single blowup over the past year, from 3AC to Celsius to FTX. This, despite the fact that Alameda Research was the largest recipent of USDT.

Tether’s motto: Trust, don’t verify.

Tether’s honesty and the funds backing their token have been called into question by many, including major media outlets. It would seem reasonable to ask these questions, given Tether’s extremely limited disclosures and history of lying about said reserves.

Instead of providing more information and clarity, Tether’s response to these questions always follows a similar pattern of hysterical denial and denunciation:

Now, call us skeptical, but wouldn’t it be easier to simply show us the money?

We need Jerry McGuire in there, “show me the money, Jerry”!

Excellent report sir!