Schwab's Shrinking Spread

Charles Schwab built its business on low-interest deposits. Then deposits started bleeding as interest rates rose...

Note: We have no financial position in Schwab (SCHW). Nothing in this article should be taken as financial advice; this is presented for informational purposes only.

After the collapse of Silicon Valley Bank and Signature Bank in mid-March, depositors and investors scrambled to identify and flee other troubled banks. One surprising target for panic was Charles Schwab, the well-known brokerage firm that also owns T.D. Ameritrade. Unlike the other names in the news, Schwab is not (at least on the surface) primarily a bank. Schwab’s primary services for its customers are brokerage, asset management, and investment products.

However, Schwab also quietly operates one of the largest banks in the United States, into which it sweeps customers’ brokerage account cash. The realization that Schwab, like other banks, had significant unrealized losses on its securities portfolio led to a brief panic that the company might meet the same fate as SIVB. However, Schwab issued a statement indicating that their institution would survive a run due to ample liquidity:

We have access to significant liquidity, including an estimated $100 billion of cash flow from cash on hand, portfolio-related cash flows, and net new assets we anticipate realizing over the next twelve months. We believe we have upwards of $8 billion in potential retail CD issuances per month, plus over $300 billion of incremental capacity with the Federal Home Loan Bank (FHLB) and other short-term facilities – including the recently announced Bank Term Funding Program (BTFP).

In an interview with the Wall Street Journal around the same time, Schwab’s CEO made the bold claim that they could pay out 100% of deposits without having to realize any losses on their securities portfolio:

“There would be a sufficient amount of liquidity right there to cover if 100% of our bank’s deposits ran off,” said Walt Bettinger, Schwab’s co-chairman and CEO, referring to the company’s banking unit. “Without having to sell a single security.”

While he was correct in the short term, Mr. Bettinger’s statement hints at the longer-term problems that Schwab now faces. Schwab has profited on the spread between near-zero interest deposits and higher interest securities, a strategy that accounted for nearly 25% of net revenues at the end of 2022. However, Schwab has been bleeding the low-interest deposits that made their current business model viable. As Schwab races to replace these funds with higher-interest alternatives, the company is dismantling one of the key foundations of its business model. While the future is uncertain, it seems likely that Schwab is going to have a pretty rough 2023…

Schwab’s balance sheet suffered as interest rates rose

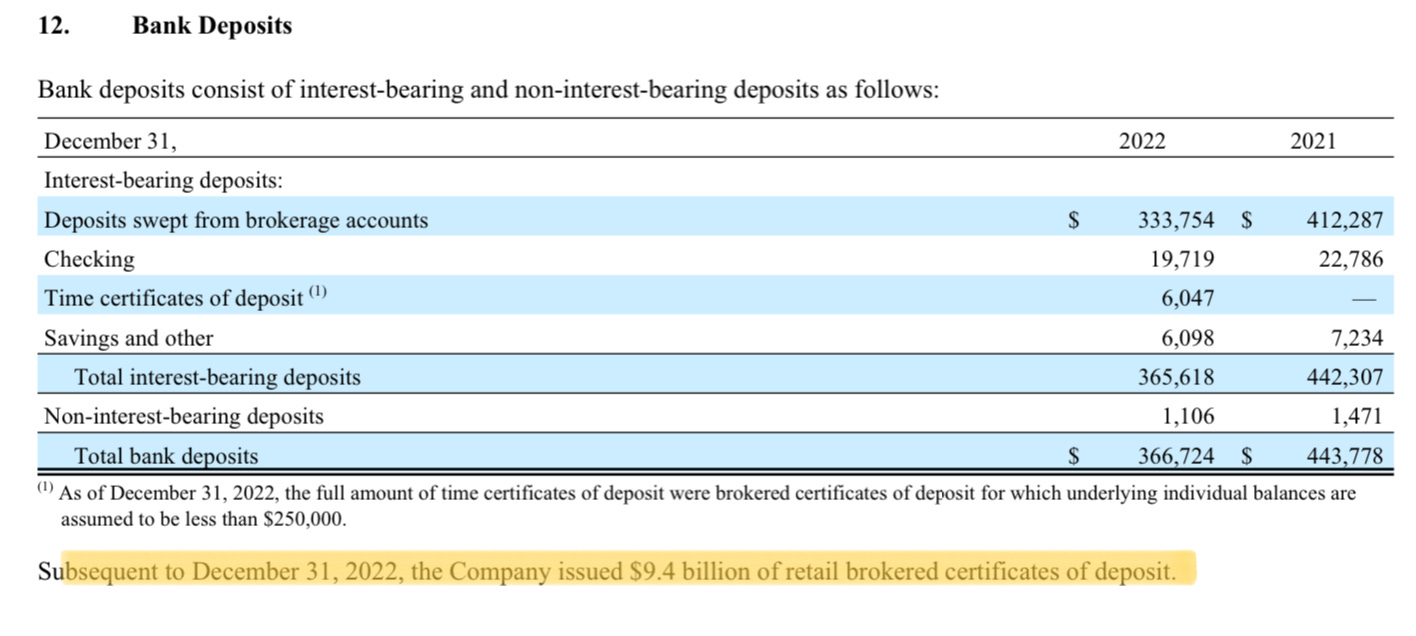

In addition to operating their brokerage and investment advisory services, Schwab owns three banks that it uses to hold brokerage clients’ cash. Dollars in brokerage accounts are “swept” to Charles Schwab SSB, Charles Schwab Premier Bank, and Charles Schwab Trust Bank. Between these three banks, Schwab held over $366 billion in customer deposts, with over 90% of the deposits held at Charles Schwab SSB (as of December 2022).

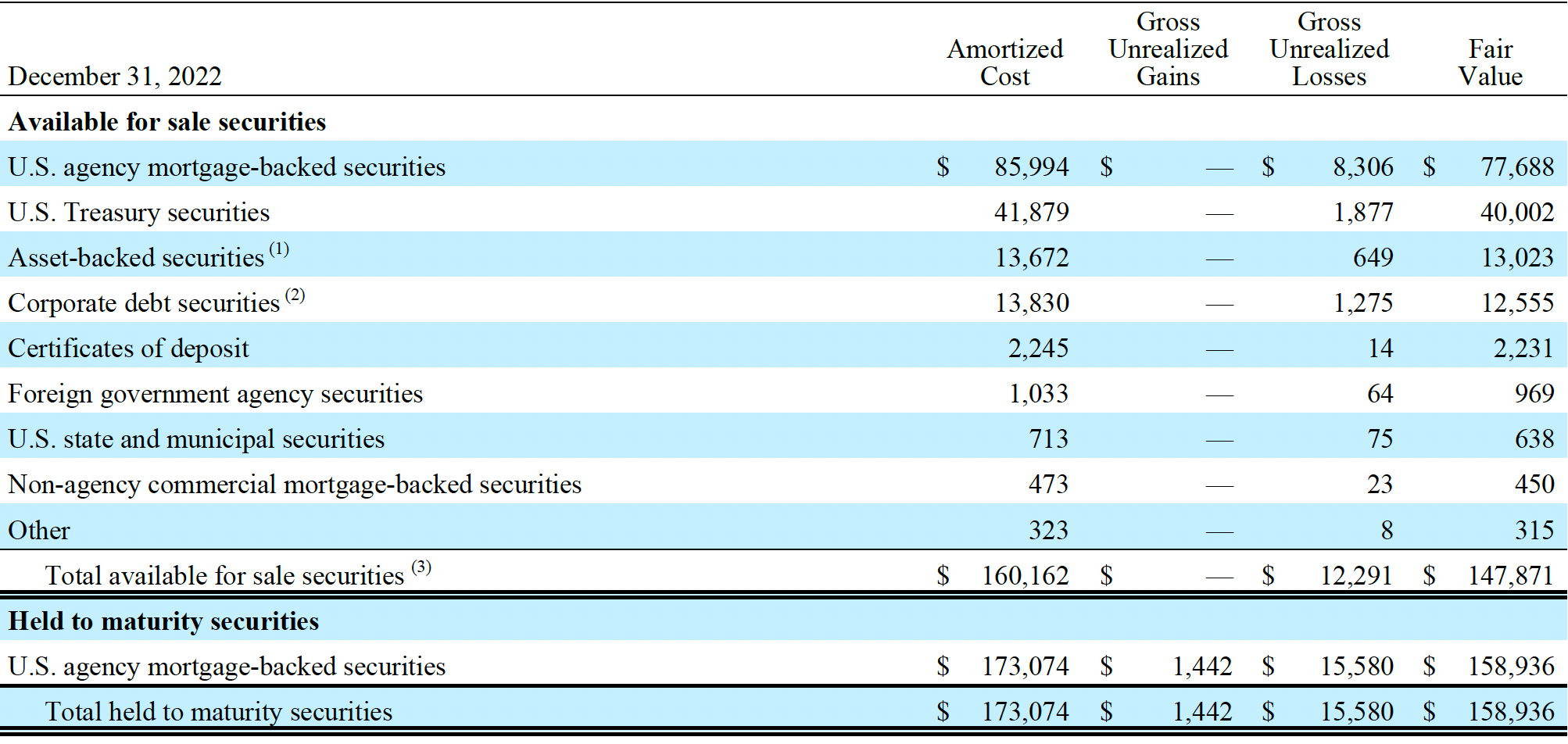

Schwab has deployed these to purchase large quantities of mortgage-backed securities and Treasuries. By December 2022, Schwab held mortgage-backed securities totaling $259 billion or 78% of their securities portfolio. Of the $333 billion in securities held, approximately 75% have maturities exceeding five years.

Note the second column: Schwab had gross unrealized losses of close to $27 billion on these holdings during 2022. As interest rates rose, the market value of their relatively low-yield and long duration debt instruments plummeted. Techically, this means Schwab saw comprehensive loesses of $14 billion in 2022:

Now, as Schwab has previously stated, one must be careful when accounting for unrealized losses on debt securities. If the company can find alternative sources of liquidity to pay out withdrawals, they can avoid realizing these losses. As long as the securities are held to maturity, there will be no real loss to the company.

We agree that Schwab will probably not be forced to realize these losses. Instead, it is the general shift in funding costs that represents a longer-term threat to the company’s business model.

Schwab was bleeding deposits well before the banking panic.

As described above, during the last three quarters of 2022 Schwab saw significant deposit outflows totaling some $77 billion. These nearly wiped out the deposit gains the firm saw over 2021 and early 2022. Overall, the company saw $105 billion leave when payables to brokerage clients are included:

The Company’s consolidated Tier 1 Leverage Ratio increased to 7.2% at December 31, 2022 from 6.2% at year-end 2021. This increase resulted primarily from lower bank deposits and payables to brokerage clients, which decreased by a total of $105.3 billion, or 18%, in 2022 due to client cash allocation decisions resulting from the rising interest rate environment….

Schwab has relied on the Dallas FHLB to make up the difference. The bank made ample use of the FHLB lending program to cover the lost deposits. By December 2022, Schwab had $12.4 billion in FHLB loans outstanding, compared with zero FHLB loan balance in the prior year. In the first two months of 2023, Schwab went back to the FHLB to borrow an additional $13 billion, bringing their total FHLB loans to $25.4 billion as of February. These loans carry interest rates near 5%. Notably, Schwab was already the largest borrower from the FHLB in December:

At December 31, 2022, the Bank had advances of $10,000,000,000 outstanding to its largest borrower, Charles Schwab Bank SSB, which represented approximately 14.4 percent of total advances outstanding at that date. In addition, at that same date, the Bank had advances of $2,400,000,000 outstanding to Charles Schwab Premier Bank, an affiliate of Charles Schwab Bank SSB, which represented approximately 3.5 percent of total advances outstanding as of December 31, 2022.

Schwab also used repurchase agreements, in which short-term loans are advanced by other financial institutions against investment securities, to borrow $4.4 billion in 2022. In the first two months of 2023, Schwab used repo agreements to borrow another $3.4 billion. Between FHLB and repos, Schwab reported borrowing $33.2 billion.

Finally, Schwab has gone to the certificate of deposit market to replace lower-interest deposits. Over 2022, Schwab added $6 billion in CD’s. In the first two months of 2023, the firm issued another $9.4 billion in brokered CDs, bringing the total to over $15 billion:

In total, this means that Schwab had raised over $48 billion in combined FHLB advances, repos, and CDs by February 2023.

Schwab depends on interest income for revenue.

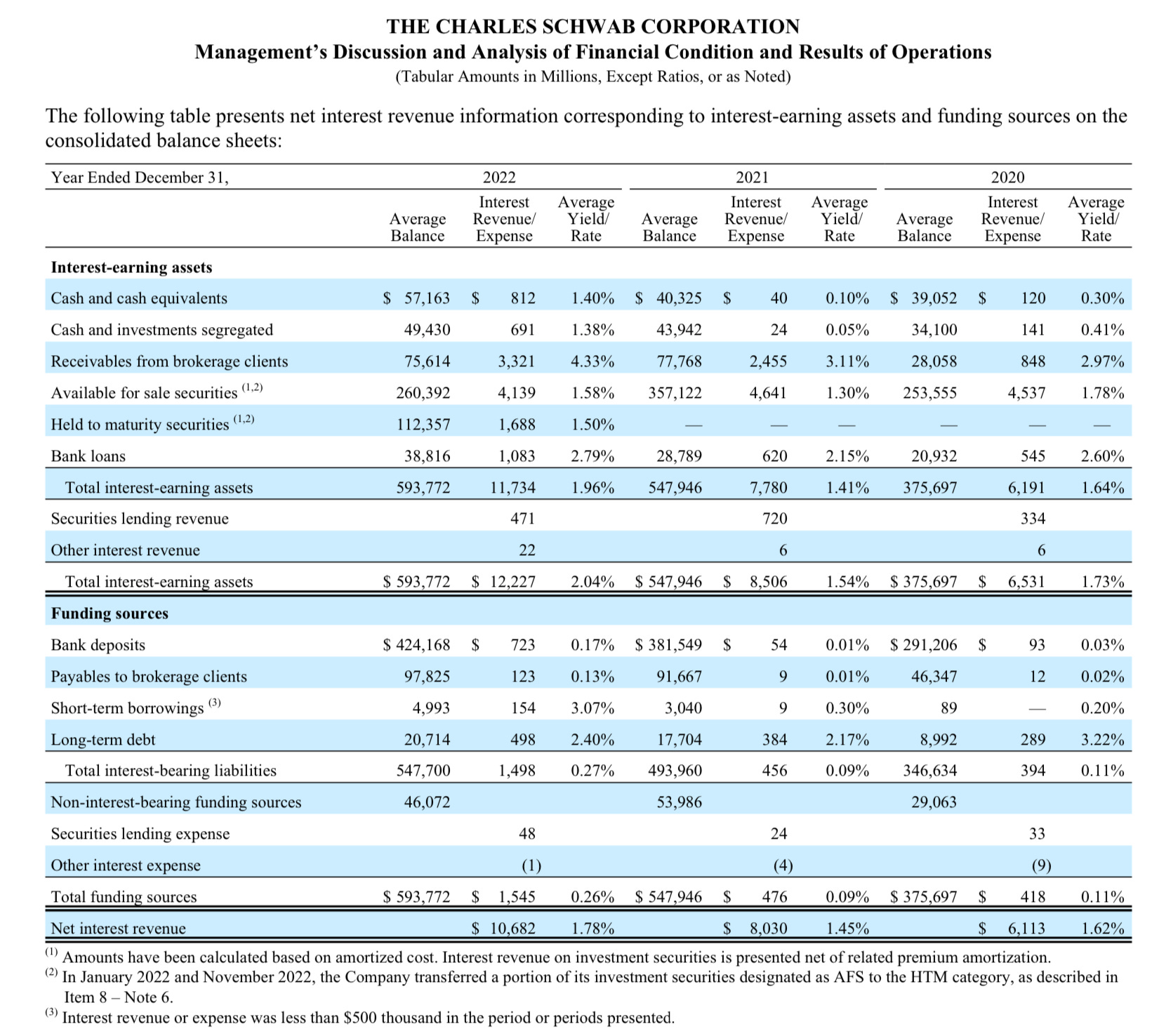

Schwab derives a significant portion of its revenue from interest on longer-dated mortgage-backed securities and government debt. In total, interest revenue accounted for slightly more than 50% of Schwab’s net revenues in 2022. Roughly 48% of interest revenue was derived from their AFS and HTM securities assets, which are earning an average rate of <2%.

It’s worth noting that net interest income was the sole driver of revenue growth in 2022:

Average interest rates paid on Schwab’s deposits were a paltry 0.17% over 2022. This compares to average rates of 4.88% on recent FHLB loans, 4.99% on repos, and 4.7% for retail certificates of deposit. In other words, these alternative sources for liquidity cost about 28 times more than Schwab’s lower cost deposits. This is also roughly three times higher than their average yields on both AFS and HTM securities. So, for every $1 of deposits Schwab replaces with higher-cost alternatives, they wipe out over $2.50 worth of interest on their securities holdings.

As of the date of the 10k filing, Schwab had some $48 billion in FHLB loans, repos, and CD’s earning around 4.8%. Assuming this level of borrowing remained stable throughout 2023, this would cost roughly $2.3 billion and eliminates a significant portion of their earnings from their securities portfolio.

It is somewhat difficult to ascertain the contribution of different company units to net income, as Schwab’s 10k doesn’t break operational costs up by segment. However, according to FDIC filings, Charles Schwab SSB (the largest of Schwab’s three subsidiary banks) generated $3.1 billion in net income in 2022. Schwab Premier, the second-largest subsidiary bank, generated another $286 million in net income. If this carries over directly into Schwab’s net income, this means that one third of Schwab’s pretax net income ($9.4 billion) is attributable to these banking units.

It is worth noting that Schwab’s operational costs should remain stable despite these changes in interest rates. Costs will remain the same while a key profit center gets squeezed…

Things have not gotten better since February.

As shown above, Schwab had been bleeding deposits throughout 2022. We don’t have the numbers for Q1 2023 yet, but Schwab’s recent public statements confirm that withdrawals have not abated. Per their press release on March 17:

Client bank sweep cash outflows in February were about $5 billion lower than January and March month-to-date daily average outflows are tracking consistent with February. Importantly, these outflows reflect a continuation of client decisions to reallocate a portion of their cash into higher yielding cash alternatives within Schwab. Based on our ongoing analysis of these trends, we still believe client cash realignment decisions will largely abate during 2023.

This statement is notable for the information it does not include. For example, how did withdrawals in January 2023 compare to withdrawal rates in 2022? If we conservatively estimate January withdrawals were equal to the average over the prior three quarters, Schwab would have lost another $11 billion in deposits. That would put February at $6 billion, meaning another $17 billion fled the bank in the two months prior to the March banking panic.

This is a pretty conservative estimate, as Schwab apparently borrowed some $13 billion in FHLB loans and issued another $9 billion in CD’s through mid-February. This suggests that deposit flight may have been much higher in January than the average rate of withdrawals in 2022.

Schwab also engaged in subtle misdirection in their statement. Schwab shares that they saw “net asset growth” over the week prior to the statement:

Over the past five trading days (3/10/23-3/16/23), clients have continued to bring assets to Schwab, with approximately $16.5 billion in core net new assets for the week, demonstrating the trust clients place in Schwab.

However, this result tells us nothing about deposits, as Schwab holds a wide variety of client assets including securities. Schwab also offers money market funds that could see inflows without providing support for deposits. In the case of cash movements, $1 does not always equal $1…

So that was the situation as of March 17th. How did the rest of March go? According to Schwab’s update on April 6:

Deposit flows at Schwab Bank have remained fairly consistent during this tumultuous period. In fact, adjusting for modestly increased cash movements during the week last month following national concerns about regional bank stability, the average daily outflows were below February.

The odd wording of this statement (“modestly increased”) raises some concerns that management is trying to prepare the market for bad news in as gentle a fashion as possible. The lack of information in the statement is a warning sign: One might assume that if the detailed numbers were positive, Schwab would be willing to share specifics. Instead, they have chosen to remain as vague as possible while trying to instill confidence in their customers and investors.

So what is next for Charles Schwab?

Schwab will announce their quarterly results on April 17th. At that time, we will discover the extent of the deposit flight over the past three months, as well as the ways in which the company has managed to patch their lost liquidity. Right now, the company seems reliant on short-term fixes for a longer-term problem. We think it is possible that the company will attempt to improve its financial position through debt and/or equity offerings in the near future.

Regardless of the upcoming results, the company’s overall situation remains unchanged. Customers, acting rationally, will continue to seek higher-yielding alternatives as long as interest rates remain elevated. Schwab, in turn, will find itself forced to use high-cost band-aids to patch its liquidity issues. The company finds itself pressed between the rock of higher interest rates and the hard place of a balance sheet stuffed with massive holdings of low-yielding debt.

The only question remaining is: how hard is Schwab going to get squeezed?

Note: We would like to thank one of our readers, @shoykhet_co, for alerting us to the problems underlying the Schwab business model! It is suggestions like these that lead to our best work.

The stock is down over 40%.

I don’t disagree with the research (very well done Bubble). But some of the downside is built in.

If their user deposits slow/ interest rates level off, the stock might be a buy.

Great article. I am in agreement that Schwab’s profits will be squeezed really hard. However, what seems to be missing from the analysis is the fact that under the new BTFP there will liquidity for any modest run on assets? The Federal Reserve will lend at par so no need to sell those T Bonds at a loss to the market? Did not the Fed just effectively back stop the whole U.S. banking system? Thank you.