The Binance Scam Chain

Is the Binance Smart Chain the OneCoin scam with extra steps?

For a brief time, Dr. Ruja Ignatova was one of the most well-recognized figures in the cryptocurrency industry. Her product, OneCoin, was advertised as the “Bitcoin killer.” Using multi-level marketing (MLM) tactics, OneCoin managed to pull in billions of dollars from investors over a couple of years. Unfortunately, there was a major problem with Ruja’s narrative: OneCoin had never actually created any blockchain technology. It turned out that the tokens they were selling didn’t even exist in the ephemeral “it’s on-chain” sense; these were literally nothing more than numbers on a screen.

Of course, crypto detractors would argue that there is little difference between the OneCoin scam and other cryptocurrency offerings. In both instances, investors receive nothing more than digital trinkets with no claim of practical significance. However, it is fair to say that blockchains offer certain advantages. A blockchain is a decentralized and immutable record of every transaction completed on the chain, allowing for a high degree of confidence in the records on said chain. Users of the blockchain can trust that the records are accurate because no one entity controls the records and it is impossible to alter those records. At a minimum, when purchasing a “real” blockchain token you at least know your asset is being tracked on a secure and accurate ledger.

The most egregious part of the OneCoin scam wasn’t the standard “fraud” and “pyramid scheme” aspects that are shared with so many other crypto products. It was the fact that OneCoin didn’t even meet the minimal standard of selling a “real” cryptocurrency.

In 2019, Binance created its own alternative to compete with the dominant Ethereum blockchain. Binance copied the code from two previous blockchains, Cosmos and Ethereum, to create an integrated pair of chains commonly referred to as the “Binance Smart Chain.” The Binance Smart Chain is “proof-of-stake,” meaning that validators (the transaction processors/recorders) must buy and “stake” the blockchain’s governance token to become validators and receive transaction fees. One chain, called the Beacon chain, serves as the “governance” portion of the Binance system. The second chain, the BNB Smart Chain, hosts smart contracts and the majority of the actual activity running through the Binance chains.

This might seem complicated. A “tradfi” way to think of it: Being a validator is like owning stock in a company. To get dividends from the company, you must also lock your shares up in an escrow account (“governance”).

Binance issued the “BNB” token to serve as the governance token for validators on the Binance Smart Chain. Subsequently, BNB’s price skyrocketed with the market cap for the token maxing out around $110 BILLION in 2021. Today, BNB is roughly 62% below its all-time high. While this might sound bad, BNB has actually outperformed most other cryptocurrencies. For example, Bitcoin is 76% off its ATH, while Ether is 74% off ATH.

The Binance Smart Chain and BNB are cornerstones of the Binance empire. However, recent analyses have called almost every aspect of this blockchain into question. It turns out that, like many things with Binance, a closer look reveals cracks within the façade. The vast majority of BNB tokens appear to be owned directly by Binance, and market analysis suggests that the price has been artifically inflated. Billions of dollars in purported stablecoins pegged to the U.S. dollar on the BSC were not backed with real assets for weeks at a time. The code base for BSC is not open source and appears to be controlled directly by Binance employees. And most importantly, a deep dive into the Binance Smart Chain suggests that it might not function like a blockchain at all…

Binance owns 70-80% of BNB market cap, and the price appears to be manipulated

BNB is the fifth-largest cryptocurrency with a market cap of $42 billion. Based on Binance’s own public records, they directly own between 70-80% of the total BNB. The blockchain analyst @cryptohippo65 examined Binance’s proof of reserves information to determine the allocation of BNB across both Ethereum and Binance blockchains. Cryptohippo65 discovered that the vast majority of BNB on Ethereum and the BSC were likely attributable to customer holdings. This accounted for around 15% of the circulating supply:

However, nearly all of the BNB on the “governance” chain for the Binance blockchain, called the Beacon chain, appears to be owned directly by Binance. This can be determined by a simple process of elimination: Binance does not include these addresses in their customer proof of reserves address list, yet they clearly control these addresses.

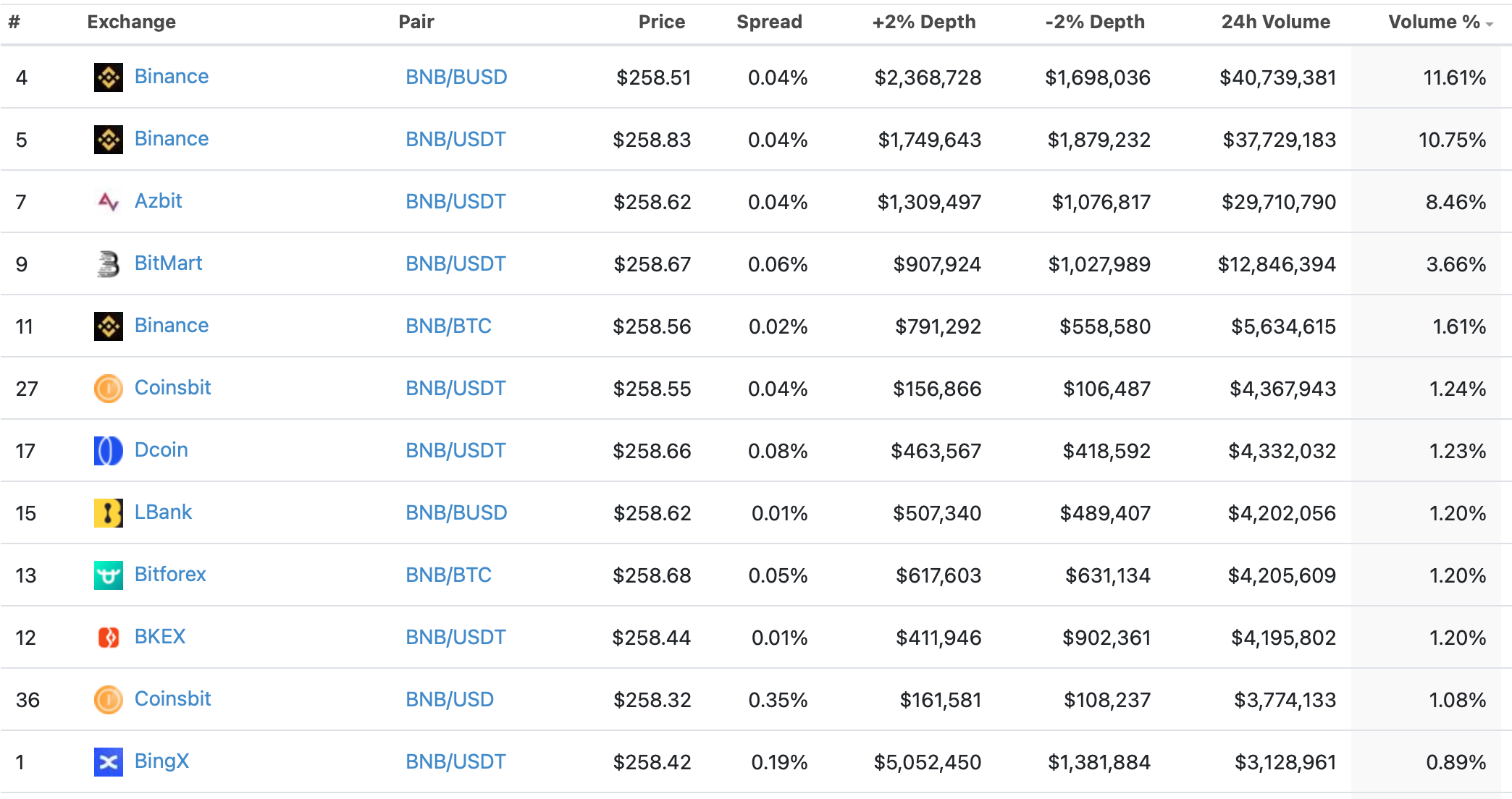

This means that Binance is holding somewhere between $28-32 billion worth of BNB on its balance sheet. Yet BNB’s price is not determined independently of Binance itself, as Binance (unsurprisingly) hosts the largest trading pairs for BNB. Notably, the next-largest spot pairs are hosted on relatively small and questionable exchanges:

Based on data from the last 30 days, the ratio of daily spot trading volume to market cap for BNB was roughly 1%. This is significantly lower than the average ratio for Bitcoin (5.4%) or Ether (3.0%), indicating that BNB liquidity is markedly lower than other major cryptocurrencies. The true BNB volume is likely much lower since a large fraction of this alleged volume is reported by highly questionable microexchanges.

Thus, like the infamous FTT token that destroyed FTX, one should question whether BNB’s price reflects reality. With Binance holding the vast majority of tokens on its balance sheet, and the majority of trustworthy volume hosted on its own exchange, how likely is it that Binance could actually sell a significant portion of its BNB for dollars without crashing its price? These data indicate that BNB is just another stupid flywheel, like FTT or CEL.

Additionally, many onlookers have questioned the price behavior of BNB. The journalist and researcher Dylan LeClair has observed that the price of BNB skyrocketed in 2021 in an up-only pattern that appeared driven by a sudden and massive increase in “people” buying perpetual futures contracts on the price of BNB:

LeClair has also noted an, um, interesting correlation between the price of BNB and FTT:

Finally, cryptocurrency proponents tout decentralization as a core value of blockchain technology. However, Binance controls the vast majority of BNB on the BSC governance chain. Since BSC operates under a modified proof-of-stake validation mechanism, this means that control of the BSC is centralized in the hands of Binance itself. What’s the point of a centralized blockchain?

BSC stablecoins were printed from thin air

Binance’s branded stablecoin, BUSD, is issued by a New York-based company called Paxos. As we previously reported, Paxos provides relatively good documentation of the reserves backing BUSD.

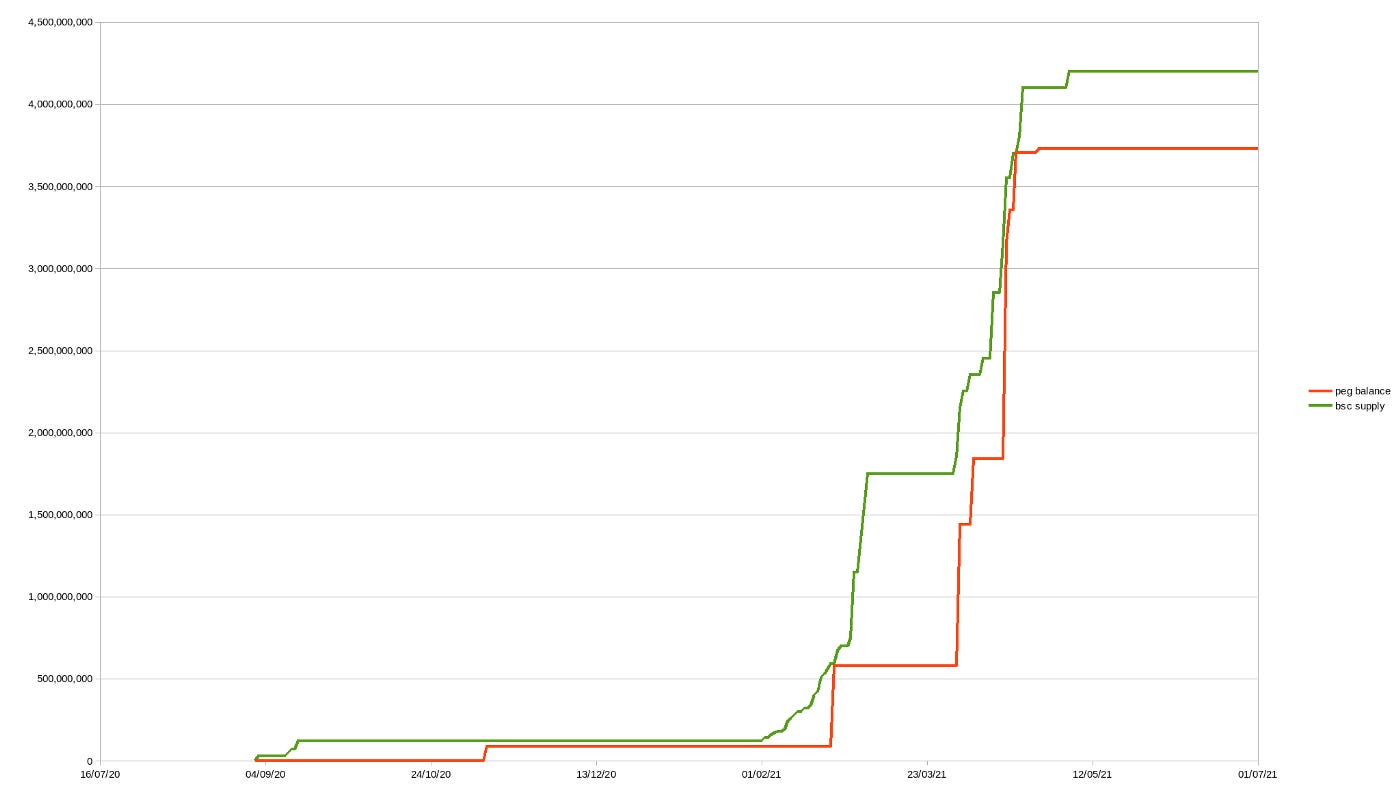

However, Binance also issues its own derivative form of BUSD on the Binance Smart Chain called peg-BUSD. To do this, Binance claims to hold an equivalent number of Ethereum chain BUSD to “back” the derivative pegged token. Consequently, the number of tokens held in their peg reserve wallet should equal the number of tokens issued on the Binance Smart Chain. Currently, there are over $5 billion in peg-BUSD on the BSC. These appear to be 100% backed today.

However, the blockchain analyst DataFinnovation went back in history to examine these peg-BUSD tokens. When he tried to match the number of pegged tokens to the Ethereum BUSD held in reserve, DataFinnovation discovered that the Binance backing wallet frequently ran at a large deficit for weeks at a time:

In other words, Binance had printed dollar equivalents from thin air. As DF notes, at a minimum this suggests incredible disorganization at Binance. DF also noted something interesting: the periods where pegged BUSD was unbacked correlated neatly with periods of time when BNB prices skyrocketed. It is almost as if Binance needed the money to raise the price of BNB…

The code operating the Beacon chain is not open source… and it might not even be a blockchain

A couple weeks ago, blockchain researcher @cryptohippo65 went digging around in the BSC explorer and discovered an interesting anomaly: There was an address holding some 22 million BNB ($5.7 billion), but there was no record of how the BNB had arrived in this address:

The missing data was attributed to an “imperfect explorer” by a Twitter user claiming to be the “Chief Scientist” for the BSC:

To check this, DataFinnovation took the step of creating his own BSC “node” and attempted to download every transaction ever performed by the Beacon governance chain. However, he ran into some interesting problems when he tried this. His attempts encountered multiple error messages that prevented a full download of the record:

panic: Failed to process committed block (285268100:BE648E40618C858CD5FEB6D83517121BAF0F9624DE7A2A6666BD5E12F8C9BB34): Wrong Block.Header.AppHash. Expected 44D7905CE27CD8035800CB05689C59FF2577F6B1A2545DDFD74B5FDEA3F8F584, got 872C99D77FB32857030F253947EC17F29A12536056F93B64F299D2E7FB24DE46

He discovered that the downloads were breaking at blocks generated near 00:00 every day.

In his excellent summary of DataFinnovation’s recent work, Patrick Tan notes the coincidence that:

Binance, the centralized cryptocurrency exchange resets its price candles at the same time everyday.

In other words, the immutable chain linking every transaction appears to mysteriously break every 24 hours. This is a problem that simply should not happen if the Beacon chain is a true blockchain. And, importantly, this error suggested that the Beacon chain must have a workaround to repair this daily breaking point.

When trying to find a solution to this problem, the BNB “chief scientist” shared a Gihub code repository for the Beacon chain. It was notable that this relevant code was added to the repository only a couple hours before he shared it on Twitter. When DataFinnovation asked about this odd fact, the chief scientist stopped responding to the thread:

This means that key information required to use the Beacon chain was not shared with the general community until people went asking for it. This is not an open source project!

After receiving this code, DF stumbled on a tool in the Beacon chain code called “state recover.” This tool allows people trying to download all transactions to bypass the errors by retroactively re-writing the history of the blockchain. This violates the core principle of a blockchain, which is maintaining an immutable record of all transactions.

As DF says, tongue-in-cheek:

If your blockchain has a “state recover tool” to rearrange hashes it may not be a blockchain. Similarly folks have been reporting problems with AppHash for years. Were we not already successfully running nodes on TRON, Huobi Eco Chain and other, um, projects with limited documentation we probably would have given up. Alas here we are.

Consequently, BSC is not a blockchain in any meaningful sense. As DF points out:

If this thing is not really a blockchain it means whoever is repairing these hashes is operating the system. We can debate how and to what degree Bitcoin, Ethereum and other blockchains are decentralized. But nobody there is repairing hashes looking backwards whereas here things look decidedly less like Satoshi’s vision.

Subsequently, the “chief scientist” reported that they had fixed this error. How they did it is still undetermined…

Is BNB just OneCoin with extra steps?

The value of BNB is, in theory, derived from its use case as the “stock” of the Binance blockchain. We showed above that, like FTT or CEL, BNB ownership is highly concentrated in the hands of Binance itself. In yet another flywheel scheme, Binance appears to have spun up tens of billions of dollars in free assets on paper. We don’t know if Binance has leveraged these tokens; their CEO insists that Binance has no loans. Regardless, it’s clear that the BNB held on Binance’s books are worth far less than what current market prices suggest.

As we have demonstrated, there is substantial evidence that there are major problems with the Binance Smart Chains as well. These include hypercentralization of chain governance in the hands of Binance, periodically unbacked stablecoins, and a closed-end project under the control of a shadow group tied to Binance. Most importantly, DataFinnovation’s analyses suggest that the BSC does not operate like a proper blockchain.

These problems suggest that BNB is little better than OneCoin. Sure, there’s a blockchain underlying BNB, but that blockchain bears no resemblance to the type of decentralized and trustless technology that attracts cryptocurrency advocates. As Satoshi Nakamoto himself said:

Digital signatures provide part of the solution, but the main benefits are lost if a trusted third party is still required to prevent double-spending.

If you need to trust CZ to move your money, wouldn’t you be better off just using a regular bank?

So, to be clear, I’ve long followed this newsletter and found it valuable. I consider this a same-side conversation

Point 1 - I'd like the article to disambiguate Binance Chain from Binance Smart Chain. In the final section they are treated equivalently. When that is done, then I think the following points could be clarified.

Point 2 - The Binance Chain problem = the back door problem (fraud).

Point 3 - The BNB concentration problem = possible negative feed-back loop (flywheel). Though to get to this point definitely we'd need evidence of loans against BNB.

I appreciate this newsletter and read each one as soon as they arrive in my inbox. I think you are right to insist on two problem points here. I think could help clarify both (this discussion helped clarify the matter for me even).

Thanks again for all your hard work!

Where there's smoke...