The Chickens are Roosting

Three more of our previous subjects face the music

Here at Dirty Bubble Media, we pride ourselves on being early to the story. In recent days, three entities we previously profiled on Substack and Twitter have finally met their maker, so to speak. In each instance, these outcomes were near-certainties, yet few people seemed to be paying attention until it was too late.

Hodlnaut puts its customers on hodl… permanently

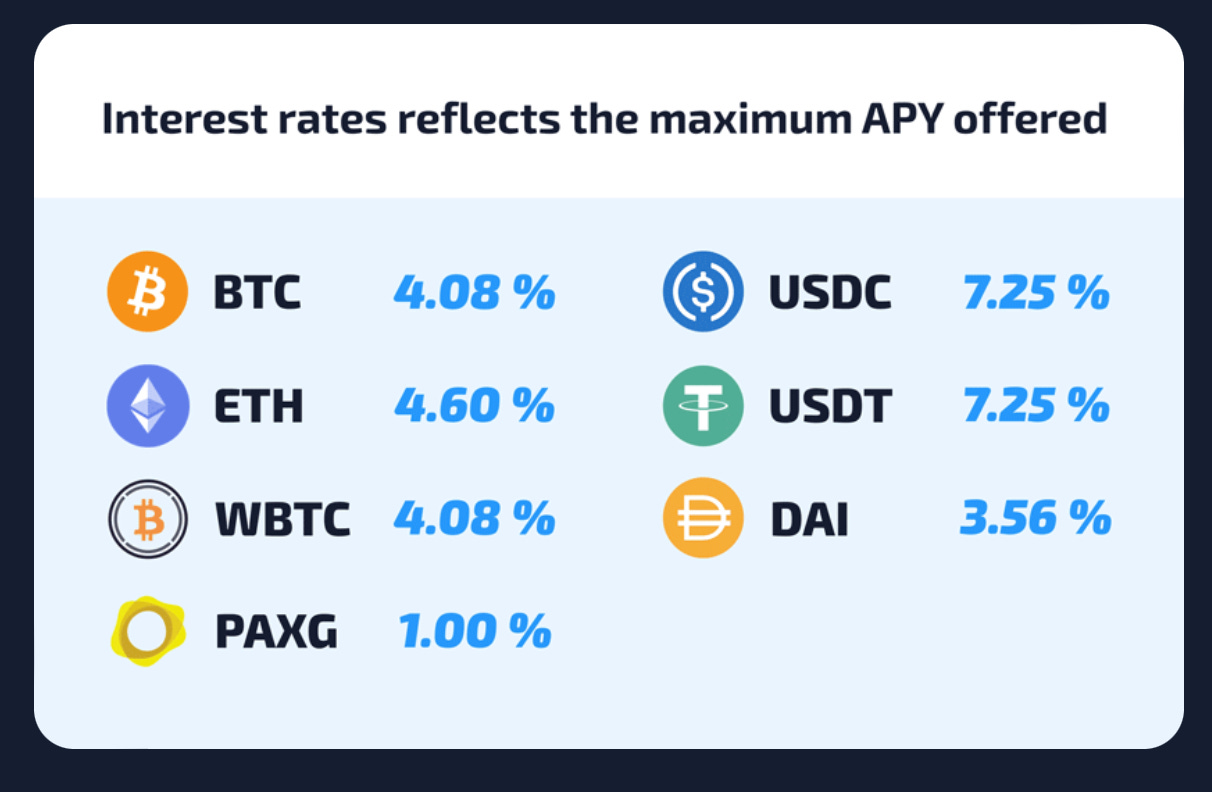

Based in Singapore, the crypto lending firm Hodlnaut claimed to manage over $250 million in user deposits. They advertised “up to 7.25% APY” on deposits on several different cryptocurrencies. Of course, the details of how they generated those returns were never quite clear…

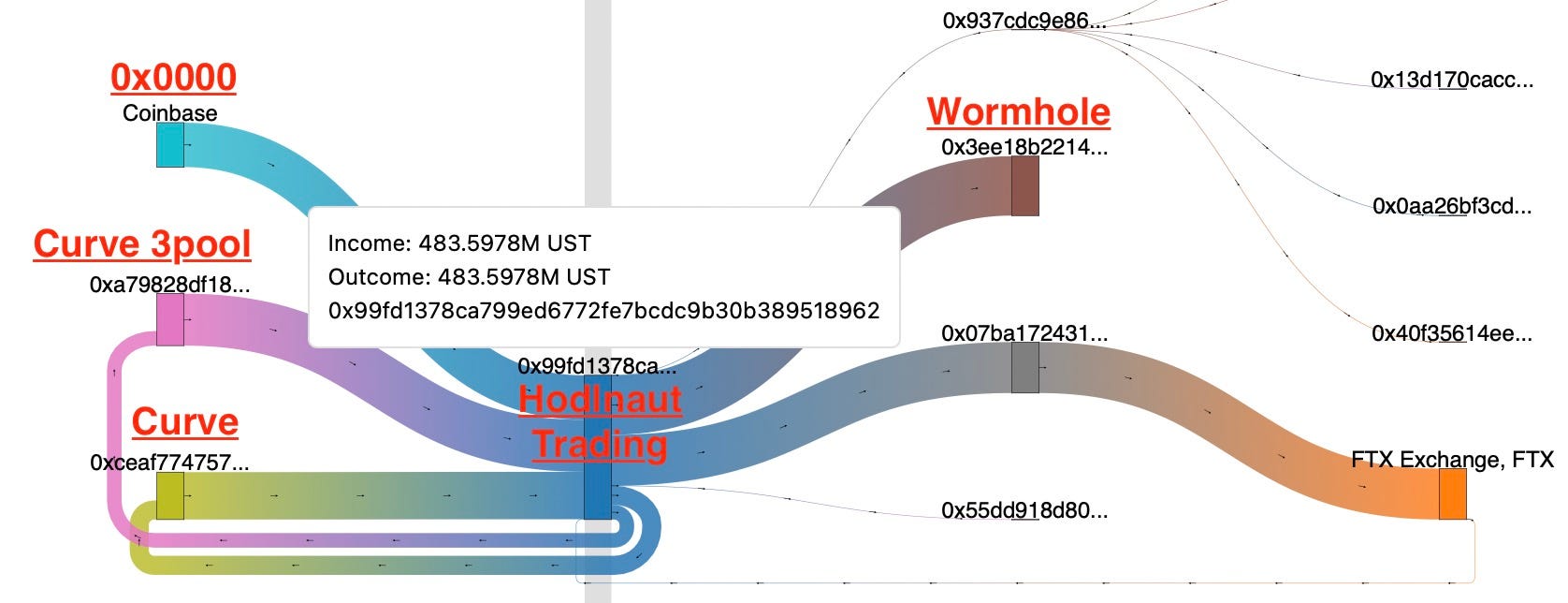

In June, we published an article demonstrating that Hodlnaut had likely suffered massive losses after the collapse of the Terra Ponzi scam:

Our report was denied by the CEO of Hodlnaut. He has since made his Twitter private and disappeared into the meta-ether. On August 8th, Hodlnaut abruptly announced that they were “pausing” withdrawals due to “market conditions.” Of course, the crypto markets had actually been going up for the past few weeks… so I wonder why they suddenly had to close their doors??

Nuri Bank, a Celsius Network feeder fund, shuts its doors

The second lending platform to fail, the German firm Nuri Banking, declared insolvency on August 9th. Several months ago, we showed that Nuri’s business model was literally “take customer’s Bitcoin and send it to Celsius Network:”

We noted that Nuri (previously called Bitwala) had originally offered a service to convert Bitcoin into gift cards. This business model failed after their partner WaveCrest was shut down for failing to follow anti-money laundering rules. Nuri then switched to crypto lending. It turns out their entire business model was:

Collect Bitcoin from customers

Send it to Celsius Network

Pay a lower interest rate to customers than Celsius and pocket the difference

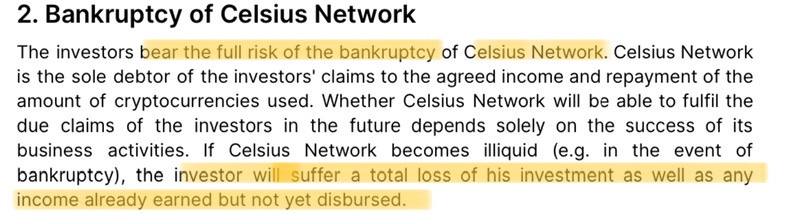

This was spelled out quite clearly in their user agreement, including the fact that their customers were exposed to 100% losses in the event of a Celsius Network bankruptcy:

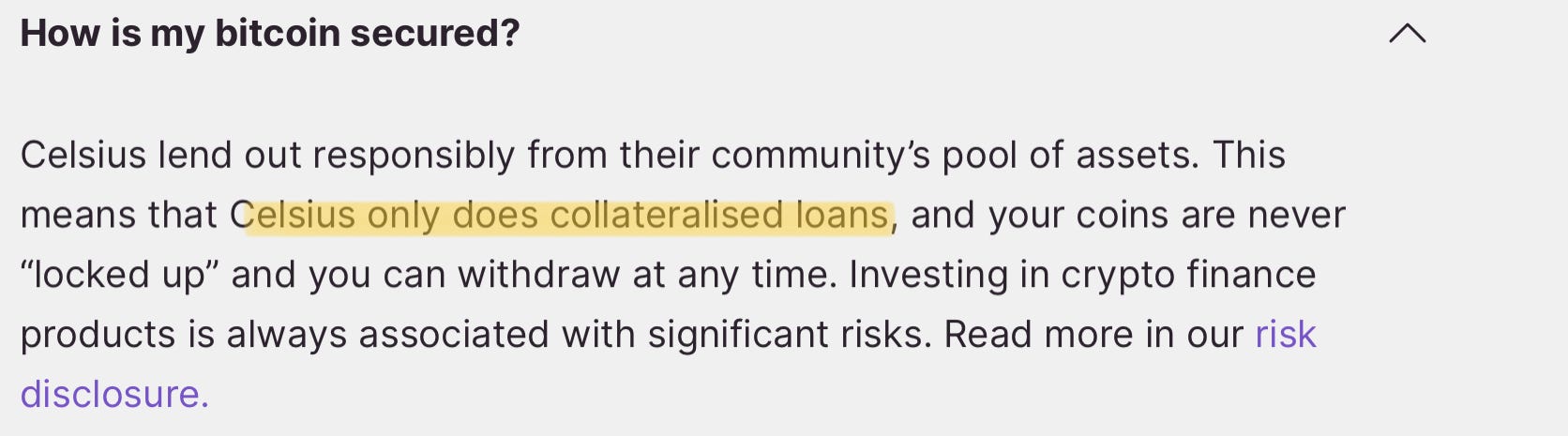

Unfortunately, their user agreement also contained lies like Celsius “only does collateralized loans” and that “your coins are never ‘locked up’ and you can withdraw at any time:’”

With their declaration of insolvency, it looks like the folks at Nuri will have to start working on their next pivot…

TornadoCash sanctioned by U.S. Government

Tornado Cash, a cryptocurrency “mixer” designed to anonymize cryptocurrency transfers on the Ethereum chain, has long been a favorite mechanism for laundering stolen crypto from various protocols. TornadoCash uses a complex mechanism to do a simple thing: Take crypto from a bunch of people, tumble it around in an opaque fashion, then allow withdrawals back out that are, in theory, untraceable:

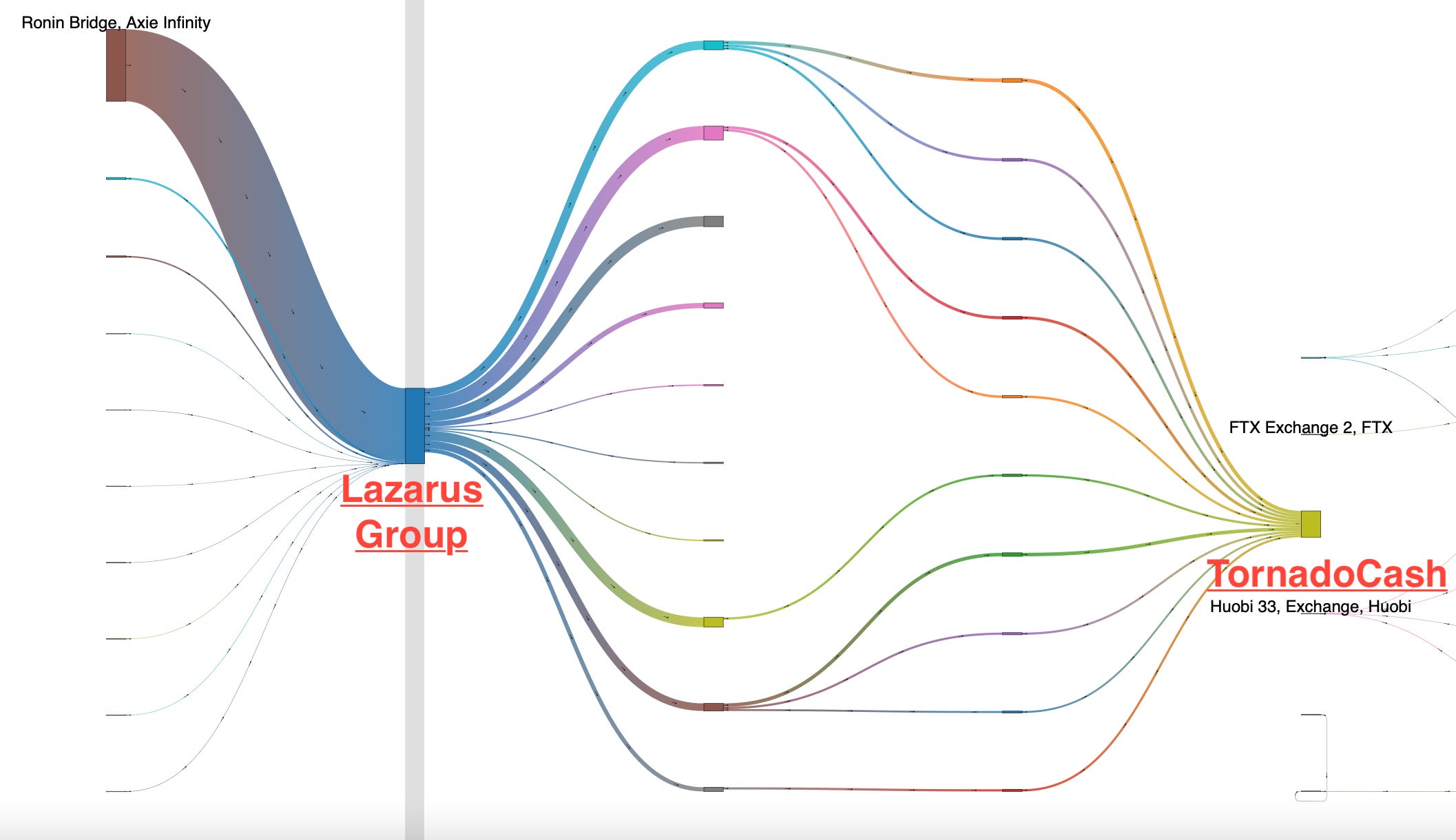

Many of the biggest thefts in the crypto-verse have used the TornadoCash mixer to prevent tracking the stolen funds. One of these was the February phishing attack on the OpenSea platform. Perhaps the largest attack ever, the $600 million heist from Axie Infinity, used TornadoCash to launder roughly 1/3 of the total haul. Unfortunately, it turns out that the hackers in this case were the infamous Lazarus Group, aka North Korea:

This, obviously, put Tornado Cash on the radar of the U.S. government. And while theft and securities fraud might not get much attention these days, it turns out that helping a sanctioned country launder hundreds of millions in stolen assets DOES merit some action. On August 8th, the U.S. Treasury Department sanctioned the Tornado Cash contract and associated addresses. A couple days later, one of the developers of Tornado Cash was arrested in the Netherlands.

Now, the question becomes: What about all of the folks who participated in the Tornado Cash “DAO" (Decentralized Autonomous Organization)? While proponents argue that the DAO members had no direct role in the implementation of the Tornado Cash contract, they did benefit directly from fees charged by the Tornado protocol. More concerning would be the consequences for “relayers,” folks who served as the intermediaries for the transfers to hide transaction fees and maintain the privacy of these transfers…

Who’s next?

So now that makes four of our previous subjects who have met unpleasant ends. Still on the docket are celebrity NFT shills who flouted FTC rules, like Justin Bieber, Reese Witherspoon, and Heidi Klum. Also, how about going after a network of scams extending from China, to Singapore, and all the way to Colorado? Or a fake company with a fake token, and possibly a fake CEO, pulling tens of millions of dollars from nowhere to buy NFTs?

I guess we will see.

And don’t forget:

We Warned You (TM)!