Why was Signature Bank shut down?

As conspiracy theories and accusations swirl, we take a closer look at the third-largest bank failure in U.S. history

Disclosure: We were short Signature Bank prior to its collapse, primarily due to concerns that will be described in this piece.

On March 13, the New York Department of Financial Services (NY DFS) announced they had removed management and placing it under the control of the FDIC:

Superintendent Adrienne A. Harris announced today that the New York Department of Financial Services (DFS) has taken possession of Signature Bank, pursuant to Section 606 of New York Banking Law, in order to protect depositors. DFS appointed the Federal Deposit Insurance Corporation (FDIC) as receiver of the bank.

The sudden collapse of Signature shocked everyone, even us. Despite being short the bank for close to a year, we thought that an outright failure was unlikely. In our conversations with traders, fund managers, analysts, and journalists, the consensus was that Signature faced significant financial headwinds and regulatory problems. Not one person we spoke to thought that the bank would go to $0.

So what happened?

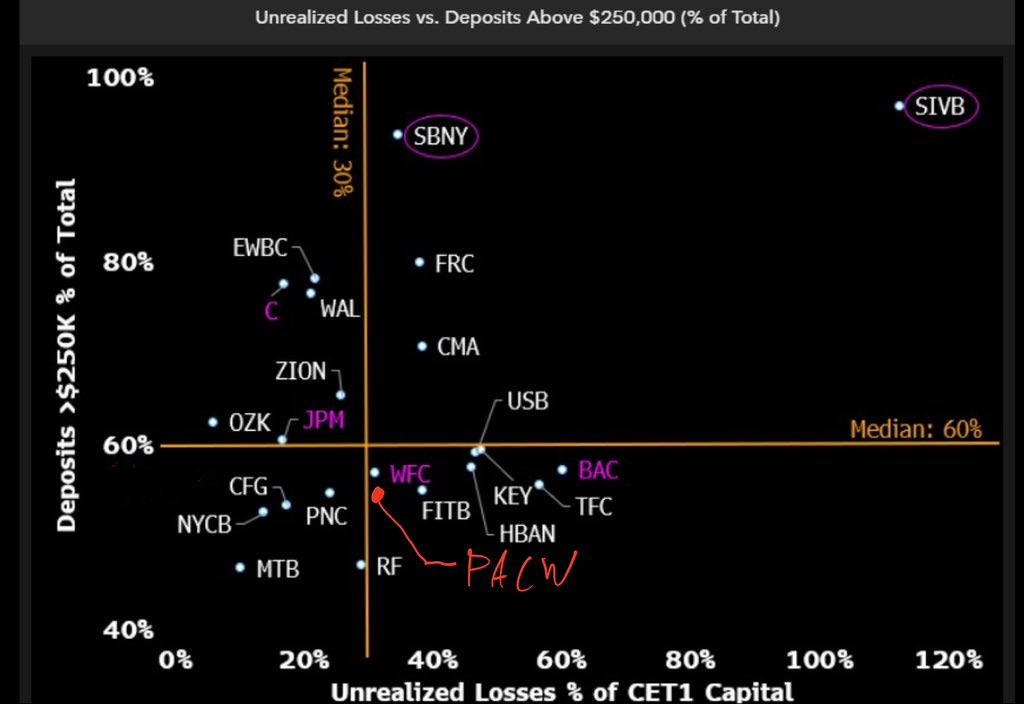

Signature’s deposit characteristics placed it at high risk for failure

However, few people expected the series of events that unfolded over the last week. Unlike Silicon Valley Bank (SVB), Signature did not have outsized unrealized losses on their balance sheet hidden in “held-to-maturity” assets. However, Signature did have an abnormally high percentage of deposits over the FDIC-insured limit:

You will note that several of the other banks with high uninsured deposits, like First Republic (FRC), Western Alliance (WAC), and Zion are also on watch lists for possible failure. FRC in particular received a $30 billion deposit infusion from multiple large banks to shore up their balance sheet; however, there is still significant concern that FRC may go under in the coming days.

Like SVB, Signature faced a run on deposits both from its crypto and non-crypto clients. With close to 90% of its deposits over the FDIC-insured limit, customers were incentivized to run for the exits when public concern rose over the bank’s financial condition. The bad news surrounding the bank and its role in the FTX scandal had already tarnished its reputation. After the failure of crypto-focused Silvergate Bank on March 8, depositors began to move for the exits. This rapidly accelerated as Silicon Valley Bank began to falter.

Signature had about $4.5 billion in cash on hand as of March 8th and $89 billion in deposits. According to Bloomberg, Signature had approximately 20% of its deposits withdrawn on Friday the 10th, with withdrawal requests piling up over the weekend:

… the DFS described “significant withdrawal requests still pending and mounting” through the weekend.

Signature lost 20% of its deposits on Friday, as clients spooked by the collapse of SVB Financial Group’s banking unit fled to larger competitors, the person familiar with the matter said.

The person, who asked not to be identified discussing a private matter, didn’t provide exact figures for how much left the bank. But Signature said in a statement Thursday that it held roughly $89.2 billion in deposits as of March 8. That would suggest approximately $17.8 billion was pulled in a single day. “

Of course, these are estimates and don’t include whatever funds were withdrawn on Thursday as the panic over Silicon Valley was mounting. We also don’t know how much in withdrawal requests piled up over the weekend prior to the shutdown.

After the failure, contradictory explanations appeared in the media…

There have been conflicting stories about the bank’s seizure, which has led to significant controversy. It turns out that one of the bank’s directors is none other than Barney Frank, the co-author of the Dodd-Frank reforms enacted after the 2008 financial crisis. Immediately after the bank failed, Mr. Frank took to the media to claim that Signature was financially sound and likely would have survived the coming onslaught of withdrawals had they been allowed to open on Monday:

“By Sunday morning, the executives of the bank believed they had satisfied the need for the data and had secured the capital from the discount window and elsewhere,” Frank said.

Mr. Frank also sparked significant consternation with his claim that the bank was shut down due to its crypto-friendly business practices:

The regulators “wanted to send a message to get people away from crypto,” Frank said in a Bloomberg radio interview Monday. “We were singled out to be the poster child for that message.”

However, the NY DFS denied this claim, stating that they had taken control due to a loss of confidence in management after they “failed to provide consistent and reliable data” as the run on deposits progressed.

Crypto advocates have taken to social media to assert that Signature’s takeover was part of an “Operation Choke Point 2.0.” According to these folks, the government is illegally pushing banks to stop doing business with crypto firms for no good reason. Even the Wall Street Journal opinion page got in on the action, wildly suggesting that the takeover was a “crypto execution.” Again, the only evidence they cite is Mr. Frank’s claims. In turn, Barney based his claims on information he received from Signature management.

So, was the takeover legitimate? And why did it happen? While we still don’t know for certain, an examination of the facts and laws involved in this situation can lead us to some reasonable possible answers.

One obvious possibility is that Signature Bank was insolvent, despite executive’s statements to Mr. Frank. If the bank was unable to make good on withdrawal requests and was poised for failure, regulators would have an obvious reason to step in. Recent revelations suggest that Signature’s real estate loan portfolio may have been more distressed than disclosed by management. This agrees with data we had obtained prior to their collapse showing that a predominance of their loans were on class C properties and often involved questionable landlords. The coming bidding process for Signature will hopefully shed more light on their financial condition.

However, New York state law describes a number of scenarios in which a bank may be taken over even if the bank is not insolvent:

The superintendent may, in his discretion, forthwith take possession of the business and property of any banking organization whenever it shall appear that such banking organization:

(a) Has violated any law;

(b) Is conducting its business in an unauthorized or unsafe manner;

(c) Is in an unsound or unsafe condition to transact its business;

…(h) Has refused, upon proper demand, to submit its records and affairs for inspection to an examiner of the department…

Criteria (h) may be the closest fit with regulators’ official statements on the seizure, as they have indicated that management failed to provide timely and accurate infomation about their financial condition. Again, this reason alone would be sufficient to satisfy legal requirements for removing management.

But, what if regulators are being deceptive, and something about Signature’s crypto business contributed to their decision? A straightforward reading of these rules demonstrates that regulators still would have been acting appropriately:

Whenever it shall appear that such banking organization has violated any law

Over the past few months, we and others shared substantial evidence suggesting that Signature Bank may have facilitated illegal activities in the cryptocurrency space. Notably, some of our assertions were backed up by a class action lawsuit filed against Signature in February for their role in the FTX fraud. In the initial filing, the plaintiff Statistica Capital explains how Signature’s know-your-customer/ anti-money laundering (KYC/AML) procedures would have alerted them to serious problems at FTX and Alameda:

As a result of carrying out its enhanced due diligence obligations… Signature knew at least the following facts, from which it had actual knowledge of the fraud:

a.There was no real separation between Alameda and FTX.Signature knew the fine details of both entities’ corporate formations, beneficial owners, management, operations, and organizational structure….

b.Alameda played a vital role in the operation of FTX….

d.Alameda and FTX lacked adequate corporate formalities…

e.Alameda and FTX lacked appropriate personnel and procedures.

Both our work and this class-action suit shared specific concerns about possible misuse of Signature Bank’s “Signet” private blockchain. The Signet blockchain functioned as an internal mechanism for 24/7/365 intrabank transfers between approved customers. The Signet blockchain was an integral piece of Signature’s crypto services and was essential for real-time settlements, particularly in the management of stablecoin reserves.

The plaintiff asserts that FTX directed them to deposit funds via the Signature Bank Signet blockchain, and that Signature employees assisted the plaintiff in connecting their Signet account to FTX’s. However, it turns out that only Alameda Research held a Signet account per FTX bankruptcy filings. Signature confirmed this fact after FTX’s collapse.

Statistica Capital asserts that they lost $300,000 as a consequence:

Since Alameda, FTX, and related entities entered bankruptcy on November 11, 2022, Statistica Capital and its majority owner have been unable to recoup $300,000 intended for FTX but actually sent or diverted to Alameda via Signet.

In other words, the combined evidence suggests that Signature knowingly allowed commingling of funds between Alameda via Signet. This is, to put it mildly, a problem.

Signature also banked another critical element of the FTX conglomerate, the Hong Kong OTC crypto exchange Genesis Block. As we and others have shown, Genesis Block (another ostensibly separate entity) processed potentially billions of dollars in crypto transactions, much of it for “garbage bags full of cash.” Genesis Block OTC was a confirmed customer of Signature and also had a Signet account. We have confirmed at least one former Genesis Block customer received wire transfers from Signature Bank to execute crypto purchases.

Outside of the FTX fraud, Signature collected a laundry list of other bad actors in the crypto space despite their allegedly strict KYC practices. Most notably, that list includes Binance’s Seychelles-based shell corporation Key Vision Development. Signature ended up debanking Binance shortly before their collapse.

In sum, a substantial amount of publicly available information suggests that Signature Bank may have broken the law. One should note that, per the NY state banking laws, the superintendent could seize the bank for “the appearance” of illegal activity.

Also of note: Shortly after Signature failed, Bloomberg reported that Signature Bank was under investigation by the Department of Justice. Based on their reporting, the DOJ’s concerns are remarkably similar to our own:

Justice Department investigators in Washington and Manhattan were examining whether the New York bank took sufficient steps to detect potential money laundering by clients — such as scrutinizing people opening accounts and monitoring transactions for signs of criminality, the people said.

Whenever it shall appear that such banking organization is conducting its business in an unauthorized or unsafe manner

The NY DFS approved Signature’s Signet blockchain in 2021 with certain provisions pertaining to its implementation and operation, including:

The approval is based on stringent requirements including to:

Implement, monitor and update effective risk-based controls and appropriate BSA/AML and OFAC controls to prevent money laundering or terrorist financing.

Implement,monitor and update effective risk-based controls to prevent and respond to any potential or actual wrongful use of virtual currency, including but not limited to its use in illegal activity, market manipulation, or other similar misconduct….

Comply with DFS’s transaction monitoring and cybersecurity regulations.

Maintain policies and procedures for consumer protection and to promptly address and resolve customer complaints.

Based solely on the public information about FTX’s use of Signet services, a reasonable case can be made that Signature had violated key features of this agreement. This would mean that Signature was no longer conducting its business in an authorized fashion.

One can also make the case that Signature was conducting business in an unsafe manner. In January, the Federal Reserve, FDIC, and Office of the Comptroller (OCC) made a joint statement about the risks of offering banking services to the crypto industry. The regulators indicated that:

Further, the agencies have significant safety and soundness concerns with business models that are concentrated in crypto-asset-related activities or have concentrated exposures to the crypto-asset sector.

In other words, federal regulators had clearly stated in January that banks like Signature were engaged in unsafe and unsound banking practices. It would be reasonable for the NY DFS to agree with this assessment considering recent events!

Conclusions: No conspiracies needed to explain the seizure of Signature Bank

We have laid out several possible explanations for the NY DFS taking control of Signature Bank last Sunday. Due to the current lack of information, these are conjectures until more details are made public. Despite the wild accusations currently running through the crypto world about the collapse of Signature, there are plenty of reasonable and legal explanations for this decision.

So what comes next? According to recent reports, the FDIC was seeking bids for Signature Bank that were due March 17th. The bidding process has caused controversy as well after Reuters initially reported that the FDIC would require bidders to “give up” Signature’s crypto business components. The FDIC subsequently contradicted this reporting. However, we would not be suprised if most bidders are uninterested in acquiring this component of the bank’s portfolio….

Barney Frank is a conman and no one should be surprised he’s involved in CraptoCurrency. That guy should have been thrown in jail for blocking attempts to regulate the housing market back in the early 2000s. Everything that guy touches is a financial disaster.

Excellent reporting. Fascinating graph. Barney Frank drank the crypto kool aid.